In a nutshell

In Part 1 of this five part series, the focus is on: (1) risks in retirement, (2) life expectancy and impact on retirement planning age and (3) annuities are insurance not investment

The three key risks in retirement are: longevity risk, inflation risk and market risk.

Annuities/pensions address some aspect of these risks, while introducing other risks; specifically annuities/pensions:

– provide lifetime income, so they are intended to protect against longevity risk (i.e. protect against the risk of running out of money)

– however, they trade-off longevity risk for inflation risk (i.e. potentially a false sense of security; just when you end up living to a ripe old age, the risk against which you bought the annuity, you find that the purchasing power of your lifetime income doesn’t buy what it used to)

– this is insurance not investment and insurance should be bought by those who need it when you can’t bear the risk, i.e. typically, insurance is bought to protect against low probability events but which have very high negative impact; insurance is not just not free but it’s not even cheap

– bring with them new risks, like: credit risk of insurance company/employer, loss of liquidity/control, no estate value.

There is no universally correct answer. There are qualitative and quantitative considerations driving a person to pension/annuity vs. lump sum (with a systematic withdrawal plan to generate income). For some the peace of mind it buys is necessary despite its disadvantages, for others who are more risk tolerant and do it yourself investors with a strong desire to leave an estate it may not make sense. It’s complicated but there are no one size fit all solutions for retirement.

This five part series on Annuity/Pension vs. Lump-Sum is composed of: Annuity/Pension vs. Lump-Sum- Part 1: Making the right decision for you which explores risks in retirement, Annuity/Pension vs. Lump-Sum- Part 2: Drivers to and away from annuitization focused on qualitative considerations toward the annuity/pension vs. lump-sum decision, Annuity/Pension vs. Lump-Sum- Part 3: Quantitative considerations focused on quantitative considerations in the decision, Annuity/Pension vs. Lump-Sum- Part 4: Monte Carlo simulation to explore retirement income trade-offs with and without annuitization where Monte Carlo simulation is used to explore the range potential outcomes given assumed Capital Market Expectations, (risk tolerance and corresponding) Asset Allocation, in the context of personal circumstances (Age, Assets, Expenses, Other Lifetime Income sources and the resulting required withdrawal rate) and compare these with annuitization. Then in order to help see the entire picture, in the 5th and final part of this series Annuity/Pension vs. Lump-sum- Part 5: Putting it all together I use the case of an 85 year old single male with a life expectancy (i.e. 50th percentile) of the order of 5 years and a 90th percentile life expectancy of about 11 years, instead of the mostly used 67 year old couple who needed to finance a potentially 30 year long retirement.

Disclosure and warning

Note that none of what follows should be construed as advice on what you personally should do in your Pension/Annuity vs. Lump-sum decision. Think of this as my (Peter’s) journey to such a decision (which it is) and feel free to consider this as only educational material on how one might go about examining such a decision in as informed manner as possible. There is no one universally right answer; what may be right for you might be completely wrong for me (and I haven’t made my decision). The future is unknown and unknowable (as most of us found out in the fall/winter of 2008/9) and the lack of transparency of financial products in general and insurance products (like annuities) in particular, make the annuity vs. lump sum decision quite difficult. Furthermore, limitations of capital market expectations, models, assumptions, simulation approaches which are used to explore possible outcomes, will almost certainly insure that the future will not unfold as expected. Unbiased professional advice (ideally with a fiduciary level of care) on such important decision is usually advisable. This further complicates matters because of potential conflicts of interest which burden many of those that you might approach for advice (from insurance salespersons who would benefit from selling you an annuity, all the way to advisors under pressure to accumulate assets under management (AUM) from which they generate fees. So keeping in mind that I am not an actuary, there is potential for errors on my part, that your personal circumstances/perspectives will be radically different than mine, and your personal circumstances/perspectives are ultimately the primary drivers to the decision.

Background

As people approach retirement are faced with the very difficult pension/annuity vs. lump sum decision, which typically was irreversible once an annuity/pension was chosen. On the other hand selecting cash-value is easily reversible, as an annuity to mitigate longevity risk may be bought at a later date (though at an unknown future price). Recently, with employers/companies trying to extricate themselves from the risks of DB plans, even those who are already receiving a traditional (DB) pension sometimes get another opportunity to re-make the decision when they get a fresh offer from their employer. I suspect that many or even most people who are members of DB pension plans, especially those which come with built-in inflation indexation and federal government guarantees, tend to choose to stay with the pension when lump sum option is offered. However, very few people voluntarily choose annuitization from a 401(k) or RRSP/RRIF type capital accumulation/decumulation plan. (Although this might change with the just announced U.S. Treasury decision to allow pure longevity insurance option in 401(k); this is requires one to annuitize only a small part of one’s assets to get some longevity protection, by the use of an irreversible deferred annuity where the income stream might start nearer to age 85, thus benefiting from annuitized assets of those who die earlier plus the tax-free growth of those assets over 15-20 years, less the frictional costs introduced by the insurance company.)

There are many learned, not so learned, and even self-serving articles/blogs on annuities/pensions (which I will use as synonyms given that we’ll be discussing primarily, though not exclusively, SPIAs (Single Premium Immediate Annuities); the main difference being in who is the provider of the annuity/pension, employer or an insurance company and who, if anyone, backstops the lifetime income in case the employer or insurance company declares bankruptcy. If you are looking for a deep dive on the subject of annuities, Moshe Milevsky spends about half of his 136 page book “Life Annuities: An Optimal Product for Retirement Income” on a review of the Scholarly Literature and a Bibliography on annuities.

There is no consensus among the experts on whether one should voluntarily annuitize or not; as I already indicated it all depends in personal circumstances/perspectives. One of the original and much quoted papers by Yaari is his “Uncertain lifetime, life insurance and the theory of the consumer” suggests that without a bequest motive annuitization is optimal. So it sounds like a no-brainer, but there is more and more new literature which raises doubts about the wisdom of annuitization; in any case, what percentage of retirees has no desire to leave bequests to children/grandchildren and/or other good causes?

Many researchers speak about the “annuity puzzle” as to why so few people annuitize voluntarily. Some recent papers however suggest that people may be acting very rationally by not annuitizing. For example a recent paper by Reichling and Smetters’ “Optimal annuitization with stochastic mortality probabilities” which concludes that “We find that most households should not annuitize any wealth. The optimal level of aggregate net annuity holdings is likely even negative”. Also Frank, Mitchell and Pfau’s paper entitled “Lifetime expected breakeven comparison between SPIAs and managed portfolios” concludes that “At what point does transferring assets to a SPIA make sense? Results suggest that only when the possibility of outliving 70 percent or more of a cohort exists, and then only at elderly ages. For ages younger than 80, assets are best kept within the family, because both inflation and possible future market returns have time to do better than SPIA lifetime sums.”

You can also read my earlier blog posts on annuities at Annuity I: What is wealth?, Annuities II: (Almost) Everything you wanted to know about annuities, but were afraid to ask, Annuities III and Annuities IV. Annuities are also included in a blog post entitled Vanguard GLWB vs. other decumulation strategies which I did when in 2011 Vanguard (US) came out with their GLWB product, where I used Monte Carlo techniques to compare various decumulation approaches using capital market expectations at the time. Then in late 2012 in the Annuity or Lump-Sum (LIF): Upcoming Nortel pensioners’ decision blog post I tried to pull together some of the factors that go into the decision.

In this series blog posts I will be building on earlier work and digging a little deeper to help acquire information that might be helpful in the decision process by further comparing to other decumulation approaches and outcomes; risk tolerance and market risk are considered in more detail.

Annuities are insurance, some need it and some don’t. Even among those who need it, often a longevity insurance or longevity annuity may be far superior. These pure longevity insurance products are not available in Canada, as yet, but have been available in the U.S. for about 4-5 years; in fact the U.S. Treasury Department has just announced that they will be permitted in 401(k)s- see the NYT’s “Longevity insurance joins menu of retirement plan options”)

Risks in retirement

The three major risks in retirement are: longevity risk, inflation risk and market risk. Depending on the approach selected for generating income during retirement one will be exposed to some or all of these (and other relevant) risks.

Longevity risk is the risk of outliving one’s assets. One of the challenges of planning our financial lives during retirement has to do with the uncertainty of how long we’re going to live, and therefore we don’t know how many years of expenses we’ll have to cover. If you had $300,000 and you knew you will die within three years then you could spend $100K/year; but most people don’t know when they are going to die so, even if you don’t want to leave an estate, you have no idea how much you can spend each year without running out of money. One place you might read that life expectancy at birth in Canada or the U.S. might be 78, or that life expectancy for a female at age 65 might be 84, or that the joint life expectancy of a 65 year old couple (i.e. the age at which at least one of a 65 year old couple will be alive) might be close to 90. What does all this mean anyways and how does it help us with planning or retirement finances?

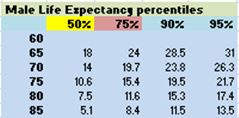

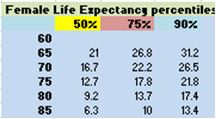

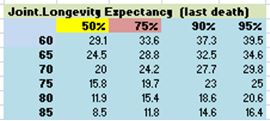

Individuals (M-males/F-females) and couples (J-joint, meaning at least one is alive) aged 65 in the general population have M/F/J life expectancies of age 83/86/89.5, as indicated in Figure 1 below. However using life expectancy as the planning age for retirement finances is a plan to fail; well at least for 50% of the population, because by definition life expectancy at some age, e.g. 65, is the number or years or age by which half the 65 year old population can be expected to have died. So life expectancy is defined as the median or 50th percentile, meaning that 50% of the group will live longer. The 75th/90th/95th percentile joint-life expectancy points for a 65 year old couple are ages 93.8/97.5/99.6! The data for the following tables was derived from the 2009 male and female Social Security Mortality Tables which represent general population statistics.

Figure 1- General population life expectancy(percentile years left to live) tables

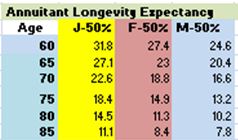

While individuals have this great uncertainty about the variability of their death around the median of perhaps +/-15 years, an insurance company which deals with a large annuitant population only has to worry about the risk that some new medical discovery might suddenly and significantly extend (median) life expectancy. Otherwise, they only have to deal with the relatively much lower uncertainty of population median age of death of +2 or 3 years as the dominant effect in calculating premiums. Insurance companies/actuaries suggest (based on data and/or assumptions) that life expectancies of the (voluntarily annuitizing) annuitant population of 65 year olds differs from the general population by having higher life expectancies; the cause of this is called adverse selection, meaning that only the healthier portion of the population would choose to voluntarily buy annuities. So while some people might think that they are betting against the insurance company as to how long you are going to live, that is not the case. Insurance companies don’t place bets; by selling annuities to thousands of people their risk is clearly defined and priced. Only the annuitant is placing a bet on the unquantifiable uncertainty of how long s/he is going to live as an individual (or couple). The following table shows the life expectancies from the so called Annuity 2000 data:

Figure 2- Annuity 2000 tables (actuarially assumed annuitant life expectancy)

Annuity 2000 life expectancies for other ages are available at source of above for single and joint annuitants. The Annuity 2000 table indicates about 2.5 years longer life expectancies than the general population table, however it’s unlikely that it is based on insurance company experience, but rather it is an actuarial projection with appropriate safety factors to protect the insurance company. In fact while it is obvious that somebody diagnosed with an incurable disease would not voluntarily annuitize, but beyond that there is no credible way to predict when a specific 65 year old will die, and whether that will be before or after life expectancy.

So, to be a little conservative, individuals/couples aged 65 might use something closer to the 75th percentile life expectancy (the age by which 75% have died) in the general population for financial planning purposes. Then the M/F/J 75th percentile planning ages might then be 89/91.8/93.8 (still leaving 25% of the population to exceed this age).

So while it’s not clear whether the Annuity 2000 (or other annuitant) life expectancies are measured or assumed/predicted by insurance companies (or actuaries working for them), what you do know is that the insurance companies will use M/F/J annuitant life expectancies starting point of 85.4/88/92.1 (perhaps with further safety factors and insurance company’s own experience) to calculate how to price annuities for large populations of 65 year olds. Therefore you can assume that annuity will be priced somewhere nearer the general population’s 75th percentile life expectancy rather than the 50th. So when you are buying an annuity, you are not only betting that you’ll outlive the average in the general population, but that you’ll outlive close to 75% of the general population. (That’s called a long-shot in my book! So much for the annuitant benefiting from adverse selection; and in any case how can 65 year old people realistically expect to predict that they will not have life-shortening and expensive health related issues at age 70 or 75 or 80, well before life expectancy of 65 year olds? Therefore, if you are buying an annuity, you better also have some substantial reserves put aside for costly emergencies, should those arise. And it not just Americans who have to worry about health expenses, according to some insurance companies even in Canada once out of the hospital after a serious illness one could have tens of thousands of dollars of expenses a year to cover physiotherapy, nursing and at-home care. Therefore, one should be building/reserving a pot of money for such emergencies as well.)

Another interesting point worth noting is that as individuals age, their life expectancy is decreasing, but by fewer years than have elapsed; e.g. general population life expectancy of a 65 year old couple is 24.5 years or age 89.5, but when they reach age 75 their life expectancy is 15.8 years or age 90.8, while at age 85 it is 8.5 years or age 93.5. This is because with increasing age additional people will have already died, and thus, from this new age looking ahead, the 50th percentile point shifts further out for those still alive. The message is that life expectancy is generally not a good number to use for retirement planning purposes at any age. Some conservative planners are using ages 95 or 100 as the planning ages of death for retirement finance, especially for couples. Notice that the 95th percentile ultraconservative life expectancy at all the ages indicates about 100!

This is where an annuity enters the picture as an insurance product which guarantees a lifetime income stream, because the insurance company’s cost is based on the still shorter (than 95 or 100) annuitant population’s median (50th percentile) life expectancy. Lifetime income guarantee sounds good as even individuals/couples planning for the longer general population 75th or even 90th percentile point would still be exposed to some extent, since the 90th percentile M/F/J general population longevity point are 95/96.1/99.6! This would suggest individuals and couples’ aged 65 would need financial planning ages of at least 89, 92 and 94 for males, females and couples, based on 75th percentile of general population (unless there are known health or longevity issues to suggest otherwise).

As already mentioned, typically insurance companies will price annuities using the so called annuitant population life expectancy tables as these are more conservative for them. Those who annuitize get the benefit of mortality credits and survivors get a return boost as they benefit of mortality credits resulting from the death of those who die earlier than assumed life expectancies the insurance company uses to price annuities. Unfortunately insurance companies also price annuities based on intermediate and long-term government bond rates currently at about 2.5%. So buying an annuity effectively locks in that low interest rate, though boosted by the mortality credits.

Obviously, somebody who was barely covering their fixed/’musts’ expenses with their un-indexed annuity at start of retirement would find themselves under increasingly serious financial pressure after a few years, as inflation starts to erode the purchasing power of the annuity income stream. This is the next key risk that will be discussed.

Inflation risk– refers to the problem that if inflation is running at 2.5%/yr (current actual is slightly lower but historically it was higher), it will erode the purchasing power of $100 after 10/20/30 years to $78/$60/$47, and we must remember that planning horizon for 65 year olds is at least about 25-30 years. In fact the primary objection of those who oppose the use of annuities is not just that they reduce/eliminate liquidity to deal with emergencies and bequests, but that they just trade off longevity risk for inflation risk (the vast majority of SPIAs (Single Premium Immediate Annuities) are nominal rather than inflation indexed payment streams. So while one won’t be running out of income with an annuity as long as one lives, but will likely be condemned to a gradually but ultimately dramatically reduced lifestyle. (Of course if you believe that we are entering a period of ultra-low inflation, or even a deflationary period, this would not be a significant issue.) So when buying an annuity one is trading-off longevity risk for inflation-risk (and who knows whether it will be more like the historical 3% or more due to the recent excessive quantitative easing, or similar to current 1-2% post recession level or we might have demographically driven deflation. If the outcome is deflation, this risk will not come into play, but history tells us that it would foolhardy to assume that.

The one factor mitigating inflation risk is that various studies suggested that spending in retirement is not increasing with inflation, as previous decumulation strategies assumed, but it is somewhat bathtub shaped (initially high due to pent up desire to travel but settles down to a lower/decreasing level until final years of life when expenses can spike again due to health and end-of-life care costs. A more recent study quantified the annual decrease in expenses to about 1% annual reduction in real terms (i.e. more than likely still increasing in nominal terms. But, I am never quite sure whether people spend less because the want to or they have to due to inadequate resources.) However it must be understood, that when one buys an annuity at around age 65 in order to explicitly secure the higher initial annual income to meet their expenses (which they can’t or won’t reduce), at the same time they implicitly are signing up to a potentially dramatic income reduction due to inflation after 10/20/30 years of 22%/40%/53% if inflation is assumed to be 2.5%/year.

Some will argue that it make sense to have more buying power while one is young early in retirement and can still enjoy that extra income, but others might suggest to take an expense reduction up front (say about 20%) and free up some investment capital which could be used to rebuild retirement pot; there is no one-size-fit-all answer to this problem. One of the best ways to protect against inflation historically has been to allocate some portion of one’s portfolio to equities. However that exposes the retiree to market risk which will be discussed next.

Market risk– refers to the risk of losing some or a significant part of one’s assets if markets drop precipitously. Specifically, someone with a 50% stock and 50% fixed income asset allocation could irreversibly lose 25% or more of one’s assets upon a 50% drop in the stock market (something like the 2008-2009 market collapse). Irreversibly because, before retirement while in the accumulation phase (i.e. while one is working and saving money for retirement), a market drop is an opportunity to make additional investment at lower prices. However after retirement during decumulation phase of the life-cycle there are no new savings to be added as the retirees are no longer working; and not only there are no further savings being added, but assets are drawn down regularly to meet retirement income needs. So for such a balanced portfolio, a 50% market drop immediately reduces assets to 75% of its previous value. Furthermore, if one needs to draw 5% of original assets each year to meet needs, and market doesn’t start to recover for 3 years, then available assets are reduced a further 15% to only 60% of their original value. That might be devastating to most retiree portfolios and retiree lifestyles. However in order to counteract inflation risk, typically retirees will need invest in some equities with their equity risk premium (i.e. a higher return) compensating for additional risk taken.

Historically equities (stocks) perform well in moderate inflationary periods. Whether one can live with the market risk if a function of one’s risk tolerance which is a combination of one’s ability to take risk (i.e. an objective measure of how much can one lose, before a dramatic lifestyle downshift is required so as not to run out of money while one lives) and willingness to take risk (i.e. a subjective measure of one’s psychological make-up and how one would react to a significant loss in assets.). So many retirees will be unable to invest in any stocks due to their low risk tolerance.

Given current life expectancies, at age 65 our assets will have to provide us with retirement income lasting 25-35 years, over which period inflation erodes the buying power of the annuity income stream; but not annuitizing would typically (though not necessarily) drive one to invest in riskier assets like stocks to overcome inflation driven income erosion (and likely meet our desire to potentially deliver a bequest.)

Annuity (or pension): Why annuitize? Is it insurance, or investment?

With an annuity one is buying an insurance (rather than an investment) product to protect against longevity risk; i.e. it is a bet that you will live longer than the average individual/annuitant of your age; and by buying that lifetime income stream you are insuring against outliving your money (but while you’ll be getting an income for life, you are accepting an inflation risk over up to 25-35 year in retirement which might erode significantly the buying power of that fixed annuity income).

An investment involves lending money to a business (interest) or becoming a shareholder of that business to benefit from the earnings of the company (dividends and/or capital appreciation); insurance involves paying a (usually) non-refundable premium which covers your insured losses should you incur a loss (in annuity the loss is the additional expenses you would incur by living longer than life expectancy+, which is paid for from the income not paid to those who live lives shorter than life expectancy.)

But we all know insurance is not only not free but, for that matter, not even cheap. While various studies have suggested that people who have a lifetime income are happier in retirement than those who have equivalent portfolio of assets, peace of mind for lifetime income comes at a price. An April 2014 Reuters article entitled “Helping clients choose annuities or lump sum” referred to a Towers Watson 2012 study entitled “Annuities and Retirement Happiness” which “found that among retirees of similar wealth and health, those with annuitized incomes were happier than those without annuities” (though the study result was a little more nuanced in its conclusion, suggesting that more wealth results in more happiness, but that the wealthier group doesn’t show much differentiation in happiness for those with or without annuities; wealthy was defined as total assets of all kinds of >$500K)

So what is nice about an annuity/pension is that you don’t have to worry about running out of money; once you hand over your pile of cash (premium), the insurance company guarantees a specified lifetime income stream which is higher than current interest rates on government bonds, but you are typically locked-into an irreversible transaction which (typically) leaves no residual assets after the annuitants die.

Some of the explicit and implicit costs of annuitization are: (1) you give up the assets (insurance premium) in exchange of the lifetime income stream so there remains less or no bequest from annuitized assets, (2) annuitizing all your assets leads to zero liquidity in case you suddenly need to access a significant amount of money, (3) annuities are priced assuming assets are implicitly invested at very low returns (intermediate and long-term government bond rates) rather than benefiting from the additional spread of corporate bonds or even equity risk premiums, (4) the buying power of the lifetime income is reduced annually by the future inflation, (5) annuities are priced on the assumption that annuitant population has significantly greater life expectancy than the general population and (6) to get the higher cash flow of an annuity you take on the credit risk of the insurance company (or employer in case of the pension) should it default and might not be able to meet its promises (In Canada there is some protection offered by an association of insurance companies Assuris and in the US there are state specific insurance schemes which protect the annuitant in case of a failure of the insurance company, again with specified caps on coverage that you must understand and manage around. In the US private sector pension are insured by the PBGC up to about $55K/year level; in Canada only Ontario has a pension insurance scheme and it’s capped at the first $12K/year of the pension.) . But if you can live with these costs, you won’t have to worry about market crashes, asset allocations, withdrawal strategies, or running out of money; you’ll only have to worry about relentlessly eroding standard of living during retirement, unless you have other assets available to compensate for effect of inflation.

Insurance also comes with other built-in costs: sales and administrative expenses, conservative assumptions on longevity, public companies need to make profit for shareholders. Load factors (the frictional costs of insurance, which is the difference between premiums paid and benefits received by all the purchasers of an insurance product) for annuities have been estimated to be in the 10-20% range according to different researchers.

When buying insurance products there are some general principles to consider, such as: (1) not buying insurance against risks that you can bear (i.e. given your current spend rate, would run out of money if you end up living much longer than life expectancy?), and (2) the most appropriate risks to insure against are those which are low probability/frequency but are very high negative impact events. (By that measure, given that by definition 50% of the people exceed life expectancy, it is not a low probability event.)

Bottom line

In a sense annuities/pensions are a perfect fit to protect against longevity risk- those who live shorter life than average won’t miss the cost of insurance, while those that live longer will benefit from the mortality credits inherent in annuities. For people who have no desire to leave an estate and are so conservative (i.e. have such low risk-tolerance) that they would only invest in government guaranteed instruments, annuities might make sense. But:

-annuities are expensive (priced on longer than general population life expectancies), and inflation indexed ones are even more so (well under 4% payouts on premium, when available)

-annuities trade-off longevity risk for inflation risk, in effect insuring that those who live longer than life expectancy will have significantly inflation eroded purchasing power just as they are expecting to benefit from having bought an annuity, even at the current 2-2.5% inflation levels which are low by historical standards

-annuities also come with loss of liquidity, insurance company or employer credit risk and annuitized funds become unavailable for bequest/estate.

-annuities are not an investment, but insurance; insurance should be bought when one can’t bear the risk and is most appropriate for low probability high impact events (living past life expectancy is a 50% probability by definition).