In a nutshell

An annually exercisable feedback mechanism in tax-deferred retirement accounts (e.g. 401(k), IRA or RRSP) is provided to assess whether a pre-retiree is on track to achieve financial objectives for retirement and identify corrective steps required to align plan execution and expectations. Shortfalls to objectives can be eliminated by adjusting: annual savings-rate, retirement age and if necessary the planned retirement expenses. A realistic plan can be converged-to by understanding the trade-offs between these adjustable variables driving plan outcome. If you are already retired, you might want to share with your still working children or friends.

The details

Once you start retirement there is little that can be done to alter the available assets; one is essentially required to work with what’s available during retirement.

However those still working, i.e. are pre-retirement, have the ability to continue to accumulate assets toward the objective of achieving desired retirement income. The questions are always: What are my objectives? Are objectives realistic given current plan? What is required corrective action?

To answer these and related questions (e.g. savings requirements, years till retirement, desired after-tax income to meet expenses), I will discuss a tool which allows you to explore your plan to achieve the retirement objectives. (People making the assumption that they can keep on working well past age 65, may be fooling themselves since forces outside of one’s control, like sickness and/or layoffs, more often than not end up governing retirement start, especially for private sector workers.)

A simple statement of a retirement objectives might be “to generate for John and Mary (both 41) the income necessary to support after tax expenses of $85,000/year starting at age 60, given an expected pension stream of $25,000/year. “

Objectives:

Current age of couple= 41

Retirement age (desired) = 60

Current Income/year (before-tax) = $250,000

Current savings rate= 20% of gross income placed into tax-deferred retirement account (incl. employer contribution, if any)

Current retirement savings (in tax-deferred account) =$450,000 (The equity in your home, with or without a mortgage, is not included in the investable/consumable assets, unless you have a firm plan to sell it.)

Reserve (for emergencies/LTC/estate in case of annuitization) = $400,000. If assets are or need to be annuitized, a $400,000 reserve is allocated for LTC, emergencies and/or estate (adjustable to suit your circumstances)

Pre-retirement asset allocation=80% stocks until 10 years before retirement, then reduced to 60% stock allocation during the final 10 years pre-retirement. (The impact of reducing stock allocation from 80% to 60% starting 10 years before retirement is about 4% reduction in expected average final retirement assets, but the lower risk would reduce asset losses should a significant (e.g. 50%+) market swoon occur during that period.)

After-tax expenses in retirement = $85,000 (This can be difficult to estimate especially when one is far away from retirement, but a simple guesstimate might be made by taking current income, less taxes (since we are looking for after-tax expenses) and expenses which might stop like: retirement savings, mortgage payments, children’s room-and-board/education; then adding in expenses which might start/increase in retirement like: more travel, higher healthcare cost. (As one approaches retirement, expected expenses need to be further granularized to understand which expenses are fixed (musts) and discretionary (wants), as this will help determine one’s risk tolerance; but this is not necessary to do this unless one is close to retirement.))

Average Tax-Rate in Retirement= 20%

Pensions (starting at 65) = $25,000

Based on these assumptions the required assets at retirement is calculated by simply multiplying the before-tax required income net of any expected pensions by multiplying by an income multiplier in the range of 30-33x for retirement ages ranging from 70-60.

Additional data and assumptions are set at default values (you don’t have to specify unless you are strongly opinionated about them, though they may change with time) are as covered in a P.S. to this blog post. (They are shown in black in the spreadsheet, so they are not required inputs, though you may change them should you be compelled to do so.)

The annual savings rate, retirement age and after-tax and pensions retirement expenses can be estimated to achieve objectives; then using the feedback built into the spreadsheet we can fine tune the plan.

Then three strategies to deliver retirement income will be compared, but Systematic Withdrawal Plan (SWP) is the base case (no Reserve is included since all assets at any point in time are available for emergencies), the other two are fallback positions using immediate and longevity annuities should they be necessary:

- Systematic Withdrawal Plan (SWP) using the Waring and Siegel approach to determine the maximum permissible draw each year; this was discussed in The only spending rule article you’ll ever need” by Waring and Siegel- A review . (Note that no reserve is allocated here in the next two approaches.)

- Plan to draw a constant amount per year from retirement until age 85 but leave sufficient funds to then buy an annuity at 85 of 1.0x the income at retirement start (modifiable, so at 1.0x it is the same whereas at 1.30x it is 30% higher to compensate for some inflationary erosion between retirement and age 85) and the $400,000 reserve (estate, medical emergencies, LTC, etc). Currently, each $1 will buy about 11¢ of immediate fixed annuity income for an 85 year old couple. Until age 85 the calculation assumes that the assets were invested at the Risk-Free Rate; no doubt many can tolerate somewhat higher risk (e.g. 20% or more stock allocation)

- Use Waring-Siegel approach to generate income from risk-free investments and at age 65 purchase an income stream starting at age 85 (i.e. a longevity insurance which in the U.S. has been available in taxable accounts for almost a decade and is now available inside tax deferred accounts (like IRA/401(k) with some caps) of the same magnitude as the maximum permissible draw at 65. Again here $400,000 assets are assumed to be allocated for reserves as in #2 above. Currently, purchased at age 65, each $1 will buy about 31¢ of longevity annuity income stream starting at age 85 for this 65 year old couple

The tool will provide the expected (not guaranteed) outcome, in each case assuming that investments are in Risk-Free asset (unless indicated otherwise, as in the case of the SWP where potential income is calculated at not just 0% but 20%/40%/60% stock allocations).

Should the calculated outcome fall short of desired retirement objectives, there are essentially three variables to adjust: increase savings rate (as a percent of income), delay retirement (to a realistic age), and/or reduce expenses.

Example

Here is the link to a tool developed to explore tradeoffs in this example. You are allowed to change ONLY the values which are shown in RED. The link opens the tool (spreadsheet) and you can see the following:

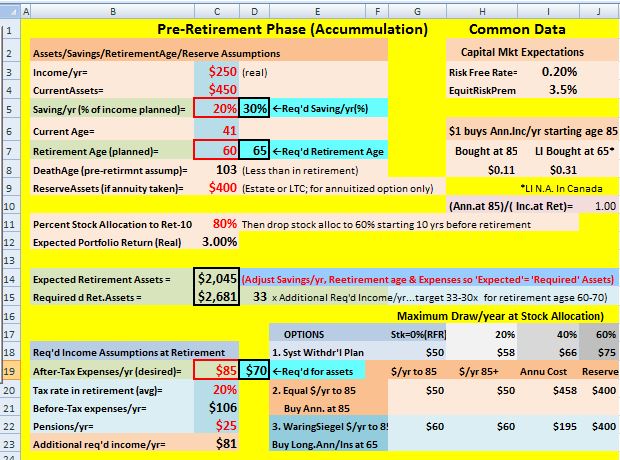

Figure 1

Inputting only the required data shown in RED, this indicates the gaps shown in the side-by-side red and black boxed cells in Lines 5, 7 and 19, that the proposed saving rate of 20% of pre-tax income/year is well below the calculated 30%/year required to retire at age 60 (the box in Line 5). Similarly, there is an asset shortfall (gap) of over $600K at the planned retirement age between the expected $2,045 at age 60 and the required $2,681 (box in Lines 14 and 15); this is the measure of whether our plan is realistic relative to our desired objective

Also note, starting in Line 18, that the $85K/year expenses in retirement gross up to $106K/year pre-tax when tax-rate is 20%, and it is reduced by the $25K pension, leaving a requirement of $81K/year to be met from the accumulated retirement assets. Given the current inputs, the $85K desired expense coverage falls well short of the estimated achievable $70k, as shown in Line 19.

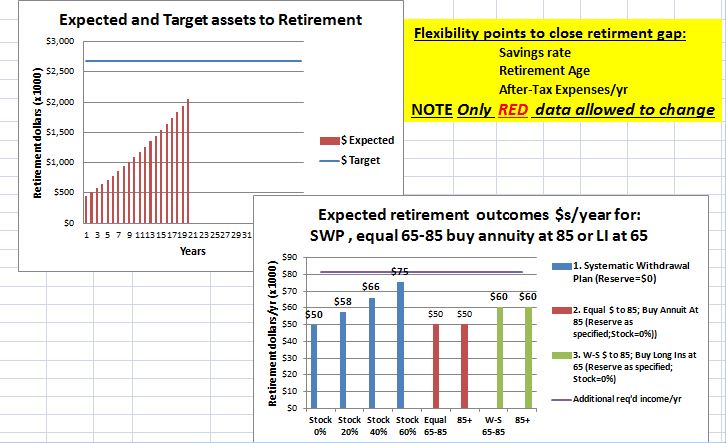

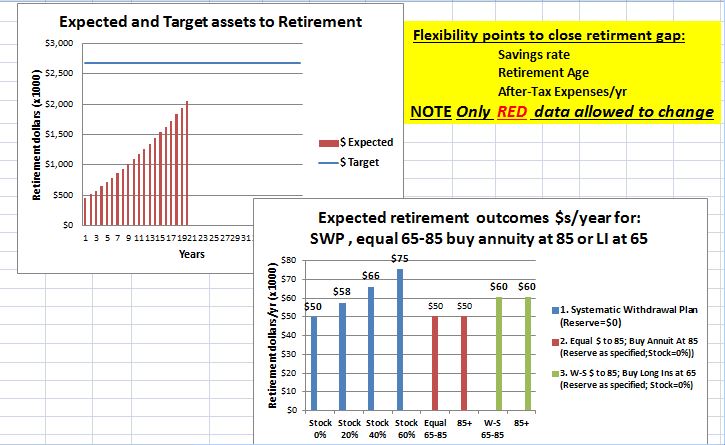

Figure 2 shows the results graphically

Figure 2

Note that the horizontal blue lines are the desired target we are aiming for, and all the approaches fall short of target (the vertical bars in the charts)

The Expected and Target assets Graph shows the about $600K shortfall at age 60 between the Target (required) assets (blue line) and the Expected assets between age 41 and 60 as indicated by the rising bars toward the blue line (objective).

The second graph (Figure 2) immediately above shows Expected retirement outcomes using the three approaches mentioned earlier: 1.SWP using Waring-Siegel to calculate maximum draw; the initial maximum draw is shown for 0%/20%/40%/60% (assuming risk tolerance permits) stock allocations (blue bars, all stock allocations fall short of desired/required $81K income from assets), 2. Equal annual income to age 85 leaving sufficient funds for immediate annuitization at age 85 plus (with a further $400K reserve) shown in brown bars (at $50K, well short of $81K), and 3. Longevity Insurance bought at age 65 to deliver income starting at age 85 (with $400K reserve) plus a W-S approach to calculate annual income (0% stock assumed here) shown in green bars (at $60K, well short of $81K objective).

We have primarily three ways to close the expected $600K gap in expected assets: (1) increase savings rate from 20% to 30%/year or, (2) increase retirement age from 60 to 65, or, (3) reduce after-tax expenses in retirement from $85K to $71K.

Any ONE of these would close the gap, but the impact may be too severe to accept. However we may be able to get an acceptable outcome by adjusting all three variables in a less dramatic manner.

Adjusting the variables: savings rate, retirement age and expenses

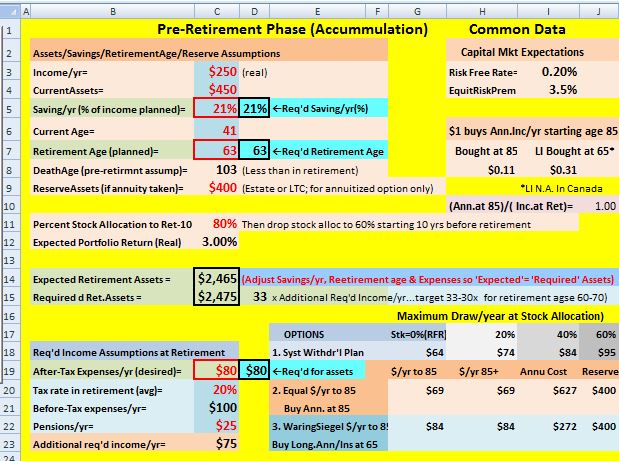

Instead let’s extract a pound of flesh from each of these three variables to reach some sort of acceptable outcome that we could still live with. Using trial and error values, we eventually arrive with one possible combination like: savings rate increased from 20% to 21% (Line 5), retirement age increased from 60 to 63 (Line 7), and (after-tax) expenses to be covered was decreased from $85K to $80K (Line 19), leading to additional before tax income (Line 23) of $75K from the tax-deferred retirement savings to cover retirement expenses now reduced from $81K/yr (in Figure 1). The results from the tool/spreadsheet are shown in Figure 3 and Figure 4.

Figure 3

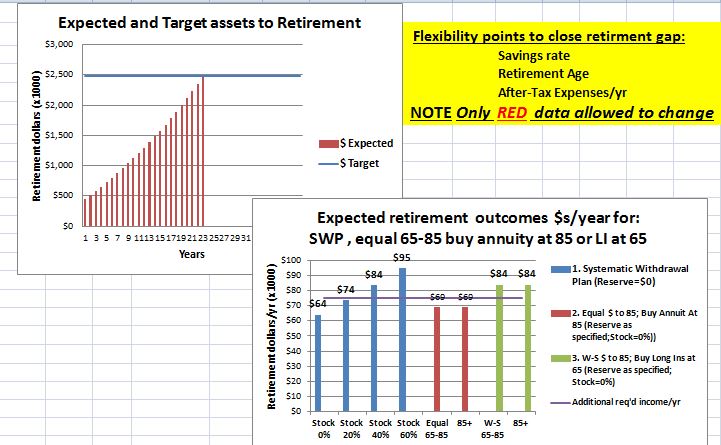

Figure 4

As you can see graphically in Expected and Target assets graph in Figure 4 above, the gap is closed to the blue line (though the blue line is a little lower due to lower retirement expenses) the brown bars now go to age 63 before gap is eliminated.

In Line 23 of Figure 3 above you can see that in retirement we’ll need $75K (instead of $81K) of before-tax income from retirement assets, in addition to the $25K pension.

Looking at the Expected retirement outcomes graph in Figure 4 that we’d have to go with at least about 20% stock allocation using the W-S based Systematic Withdrawal Plan approach (blue bars) to get almost to the new target, the blue horizontal line at $75K.

The brown bars still deliver insufficient income of $69K until age 85, when the immediate annuity will be bought. (This is the scenario where the annuity purchase takes place at age 85)

The green bars, with the longevity insurance, have the potential to deliver about $84K to age 85 (via a fixed term SWP) and then continue to do so starting at age 85+ until the last of the couple dies, from the longevity insurance income stream. (This is the scenario where a Longevity Annuity is purchased at age 65 which starts delivering annuity sourced income at age 85.) This example, as expected, shows the clear superiority of a longevity insurance/annuity provides a vastly superior outcome compared to an immediate annuity, with a 21% higher annual income stream. (Sorry Canadians, you are still out of luck if you would like to buy a longevity insurance; no visible initiative has been taken by governments or life insurance industry to try to introduce such a product- so it’s not available in Canada.) Still, the best expected outcome, for those whose risk tolerance permits, is using the Waring-Siegel approach using an acceptable level of risk; in this example a risk level as low as 20% stock is sufficient.

Bottom line

A tool to help generate, test and modify a retirement plan aimed at achieving retirement goals and objectives is provided. Ideally you’d want to run it annually to reforecast expected outcome with fresh input data. The tool is also useful as a feedback mechanism to monitor whether one is on track to achieve retirement objectives.

As you approach your retirement date, and hopefully the goal/objectives (assets/age/retirement income), then you can move to the next level of retirement expense granularity so you can size and understand the difference between “Fixed” and “Discretionary” expenses, as discussed in Stocks in retirement? Asset allocation considerations in retirement; the smaller the proportion the fixed expenses are of the annual expenses, the more flexibility (ability to take risk) one has, and thus use higher stock allocation to improve expenses outcomes. Then you can move on to use the “Stock allocation in retirement” tool which factors in ‘risk tolerance’ and ‘required returns’ to achieve objectives.

P.S.

The additional data and assumptions that are set at default values (you don’t have to specify unless you are strongly opinionated about them, though they may change with time) are as covered here as follows:

Capital Market Expectation: Risk-Free Rate (RFR) =0.2%, Equity Risk Premium (ERP)=3.5%

Income multiplier for required before-tax assets= 33

Death Age (expected at retirement) = 103

(Annuity income at 85)/(Retirement income year 1)= 1.0

Joint annuity income delivered by $1 at age 85, if bought at age 65= $0.31

Joint annuity income delivered by $1 at age 85, if bought at age 85= 0.11

{kind=link}