In a nutshell

“Insured annuity” based un-indexed income is less compelling than a systematic withdrawal of the same size from a balanced portfolio. Monte Carlo simulations suggest that even with a higher 50% indexed draw from the balanced portfolio delivering 3.5% real return, the residual portfolio value is likely to exceed the life insurance payout of the insured annuity. Even at 100% indexation of the draw the median residual portfolio can be expected to be similar to life insurance payout up to age 90. The larger partially or fully indexed income stream from the balanced portfolio with superior or similar likely residual estate outcomes at least to age 90 would likely be compelling to most, especially given the added benefit of continuous access to the assets rather than just at death. Opportunity to benefit from higher returns from future capital markets than those that would have to be locked in today with an annuity might also drive investors to choose the more flexible balanced portfolio route.

Background

A few weeks ago the Globe and Mail article “How to get more from your retirement nest egg” tabled “an idea” on how to get more retirement income; the author writes, about the superiority of a prescribed “insured annuity” for a 65 year old male over a 3.5% fixed income investment for someone with a 45% marginal tax rate. (I don’t wish to quibble about the specifics of the article but as I opined before, while annuities might be suitable for some, but better solutions are likely available elsewhere, especially for 65 year olds with little in mortality credits and much to worry about on the corrosive effect of inflation during a potentially long retirement. I am still not sold on annuities as a general retirement income strategy for most people as I discussed in the Annuity I: What is wealth?, Annuities II: (Almost) Everything you wanted to know about annuities, but were afraid to ask, Annuities III and Annuities IV .

But given my natural aversion to overpriced and often unnecessary insurance products, reading about “insured annuities” made me even more uncomfortable as this involves not one, but two insurance products: an annuity and a life insurance. The article explains how a 65 year old male who is in a 45% marginal tax bracket with $1,000,000 assets normally invested in fixed income instruments at 3.5%, would be better off buy an annuity with the $1,000,000 and simultaneously buy a $1,000,000 universal life insurance to deal with the objection that, with an annuity, the estate will wind up without any residual capital.

The numbers quoted in the article suggest that the favorable tax treatment of the income from the $1,000,0000 prescribed annuity provides an un-indexed annual income $78,000 of which only $17,000 is taxable (favorable tax treatment resulting in) thus only $7650 tax payable; the $1,000,000 life insurance would cost $30,000/year, resulting in an after tax income stream of about $40,350. The article notes that this compares very favorably with the $19,250 after tax income resulting from 3.5% interest on fixed income investments of $1,000,000. (So far so good. But the implication if an individual with 45% marginal tax rate would suggest an income of about $100,000+/year, and additional investable assets of $1,000,000; nice problem to have but very small percentage of the retiree community are in this financial situation. However for those in this enviable financial position, why would they bother to invest the $1,000,000 exclusively in fixed income investments rather than at least partially in equities as well?)

On the week that this article appeared in the Globe, I checked the highest then available annuity rates at GlobeInvestor and it indicated only $71,640/year (or 9% lower than the $78,000 indicated in the article) lifetime income . Using this annuity value the advantages of the insured annuity would be reduced $34,600 (rather than $40,350) but still well above $19,250 after tax from interest income at 3.5%.

Insurance products are often necessary, but primarily should be used when one cannot bear the financial losses associated with the risk (e.g. life insurance for the primary earner in a family with young children or liability insurance for your automobile, or disability insurance). Annuities, especially in Canada, tend to be quite expensive and while they have a place in some individual’s retirement plans, one should remember that one is essentially trading off longevity risk for inflation risk; not much of a trade-off especially for younger annuitants where mortality credits are minimal. The other annuity related issues were discussed in the above mentioned blog posts, but particularly relevant in this context is that buying the annuity today effectively locks in the current low interest rate for the life and the funds are effectively unavailable between the moment the annuity is bought and the death of the buyer.

Insured annuity vs. systematic withdrawal from balanced portfolio

There is no reason in the world why one would only compare the “insured annuity” only against investing the $1,000,000 in 3.5% fixed income investment, this is especially so for somebody who likely has in excess of $100,000/year income from other sources (to put them in the 45% marginal bracket).

So let’s look at a balanced portfolio of 50% stock and 50% fixed income. A nominal 6% portfolio return with a 7% standard deviation and a 2.5% annual inflation would likely be considered reasonably conservative by historical measures. For simplification of tax treatment let’s assume that annual interest on the 50% fixed income is earned at the 3.5% quoted in the article, while dividends of 2% are earned on the stocks in the other 50% of the portfolio. That means that the portfolio will throw off an average of 2.75% in interest and dividends which very conservatively (as the Canadian portion of the dividends would be taxed lower) will be taxed at 45% introducing a 1.25% (2.75% at 45% is 1.2375%) drag on the 6% return; i.e. we assume that the return is nominal 4.75%. Capital gains taxes will be paid at 22% rate on the portfolio value in excess of $1,000,000 when the portfolio is cashed at death (a reasonably conservative assumption since a part of the assets over $1,000,000 represent after tax dividend and interest dollars). Unlike the case of the annuity, if needed the portfolio assets are available for emergencies at any time. The comparisons are done in after tax real dollars and ratios of assets and draws in systematic withdrawals from the balanced portfolio relative to assets (life insurance) and draw (un-indexed annuity stream) for the annuity after tax and insurance costs.

With these assumptions, Monte Carlo simulations were done with the following scenarios:

Scenario 1:

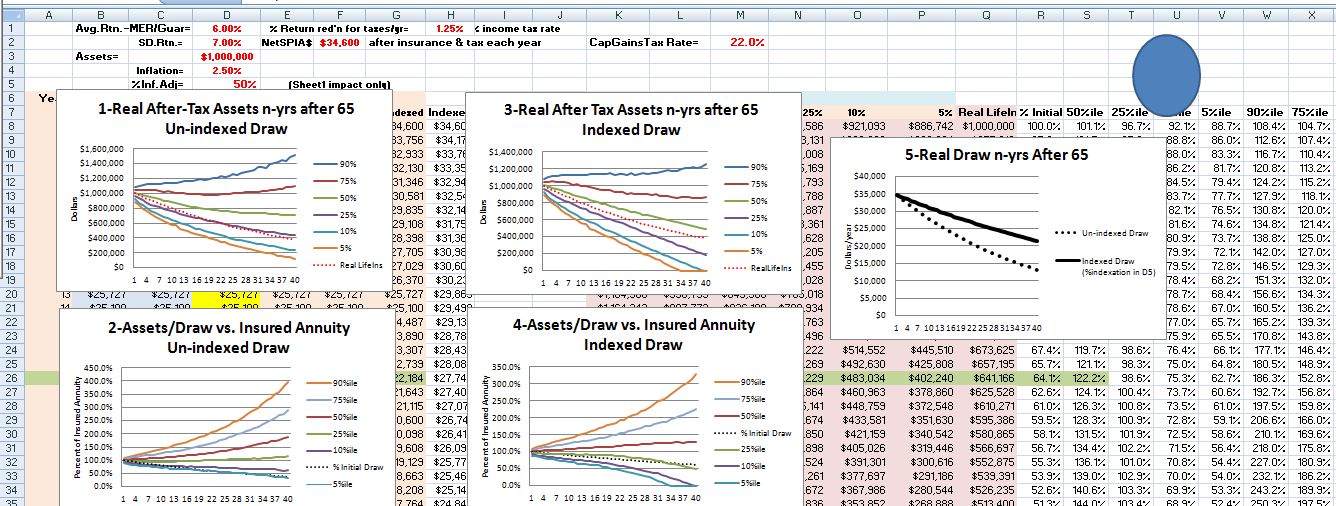

Un-indexed annuity income of $34,600and a $1,000,000 life insurance payout at death vs. $34,600 annual un-indexed and partially (50%) indexed draw from the balanced portfolio. Here the measure of goodness is the after tax portfolio value compared to the $1,000,000 life insurance payout at death.

Scenario 1

The outcome of the Scenario 1 simulation indicates that 10/20/25 years after age 65, at ages 75/85/90, the systematic:

-un-indexed draw from the balanced portfolio (i.e. the same as the income delivered by the “insured annuity”), the real value of the $1,000,000 life insurance tracks only the 25%ile portfolio residual; i.e. one has a 75% probability of a higher estate value

-even with indexation of the draw increased to 50% of the assumed inflation level, which leads at ages 75/85/90 to 10%/26% /35% higher annual income than the insured annuity, the real value of the $1,000,000 life insurance tracks only between the 35-45%ile of the after tax balanced portfolio residual; i.e. one has about a 60% chance of superior estate value

Scenario 2:

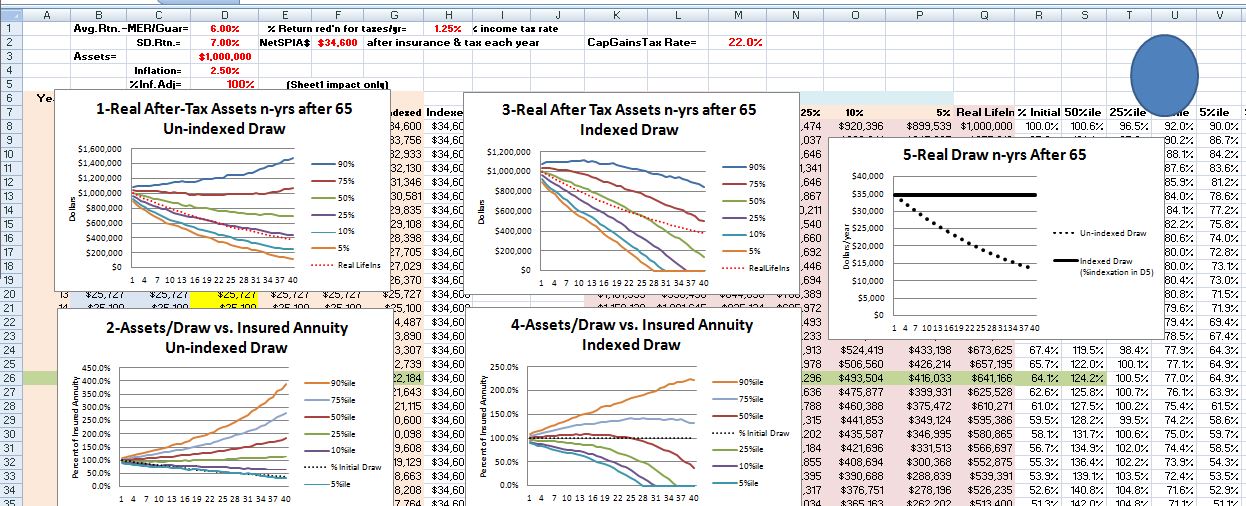

Same as Scenario 1 except when the draw from the balanced portfolio is indexed, it is fully (100%) indexed.

Scenario 2

The outcome of the Scenario 2 simulation indicates that 10/20/25 years after age 65, at ages 75/85/90, the systematic:

–un-indexed draw from the balance portfolio(i.e. the same as the income delivered by the “insured annuity”), the real value of the $1,000,000 life insurance still tracks only the 25%ile portfolio residual; i.e. one has a 75% probability of a higher estate value

-even with indexation of the draw increased to 100% of inflation, which leads at ages 75/85/90 to 25%/60% /81% higher annual income than the un-indexed annuity, the real value of the $1,000,000 life insurance tracks slightly only higher than the median (50%ile) of the after tax balanced portfolio residual until age 90, but after age 90 the high and growing withdrawal rate takes its toll on the residual portfolio; i.e. one has an expected median residual portfolio of the same size as the $1,000,000 life insurance payout until 90 even with a fully indexed draw.

Other scenarios:

A little more aggressive return assumption of nominal 7% vs. the 6% used above was explored; the 7% return with 100% indexation achieved similar after tax portfolio values as those with 6% return but only 50% indexation of the draws.

Drawing, even the higher income of $40,350 resulting from the $78,000 a year annuity assumption in the article (not available at the time the article appeared), the balanced portfolio still delivers results that would be considered preferable by many as compared to an insured annuity, though less compelling than in the case of $34,600 annual income (corresponding to the annuity quotes available at GlobeInvestor at the time or now). The median residual estate value tracks that of the $1,000,000 life insurance, until about age 87, even with a 50% indexation of the income stream drawn from the balance portfolio.

Of course, the future is unknown and your assumptions of capital market expectations might be different, but at least this begins to give us a feel for possible outcome of an insured annuity and systematic draw from a balanced portfolio given the moving parts in the scenarios.

Bottom line

Two insurance products (the “insured annuity”) may or may not be better than one (the “annuity alone”) depending on your desire to leave an estate, but the probability of superior outcomes is greater (though not guaranteed) with a systematic withdrawal from a balanced portfolio.

For people in lower tax brackets, say 30-35% marginal rates, the “insured annuity” is even less attractive.