Long-Term Care Insurance (LTCI) II- Musings on the Affordability, Need and Value: A (More) Quantitative View

(Originally posted September 2009, re-hosted in March 2012)

Last January in Long-Term Care Insurance- An OverviewI looked at LTCI policies. I promised at the time that I’ll do another more quantitative blog on the subject “shortly”. Since last January much water flowed under the bridge. The impetus needed to come back to look at LTCI in a more quantitative way, was provided by questions on LTCI from a friend and reader who started exploring his potential need for LTCI. If you are interested in LTCI sufficiently to read this article (may be hard slogging), I recommend that you first read the overview blog.

In a nutshell

Even after looking at specific examples of LTCI policy pricing and benefits, not much has changed from my conclusions in the earlier blog. I still won’t tell you to rush out to buy. Having an insurance company pay for some of our long-term care costs that (according to assorted published data) about 43% of 65 year olds will need at some point during our lives certainly sounds very attractive for our peace of mind. However, would you buy insurance where:

-Premiums: (i) are expensive (50% load factors- i.e. for each $1 of premiums collected only $0.50 is paid out in benefits), yet (ii) you don’t know how much more expensive they’ll get before you collect any benefits, and you’re probably unsure if it makes sense to buy LTCI in the first place

-Benefits: should you be among those who need long-term care, you are not sure if and when you might qualify, or even how much of the long-term care cost will be covered

-Complexity: LTCI policies are not standardized; they are difficult (perhaps impossible to most) to fully understand and may be open to interpretation by the insurance company which wrote the policy and possesses asymmetric information

-Value: not clear if the asset protection received justifies the investment

If you still think that your “peace of mind” demands that you buy an LTCI, then consider:

-a joint policy for an annual/total dollars usable by either

-compound inflation protection (5%), especially for younger (age <70) buyers

-longer elimination periods 0.5-1.0 years to lower premium

-benefit triggers: 2 ADLs out of 6, or cognitive impairment

-highest rated company, to increase the chance that it will be around to pay in 20-40 years

-waiver of premium (i.e. premiums stop when benefits start and/or only 15-20 years of premiums)

-capped premium levels

-non-forfeiture of policy if you stopped premiums (recall that 50% of policies lapse); perhaps automatically convert to “paid up” status

-prefer disability rather than reimbursement benefits (i.e. if hurdle met you get specified $/mo)

–combination products: life insurance or annuity combined with LTCI; perhaps ask your insurance company if they have LTCI riders to be added to these type of policies that you may already have

Or, you may get sufficient peace of mind if you put aside and invested each year the equivalent of the premiums (7% of “Total Income” during retirement) and created a personal LTC-fund that you could draw on should LTC be required; if not required then it becomes part of your estate.

Let’s look at how I came to these conclusions.

First some statistics

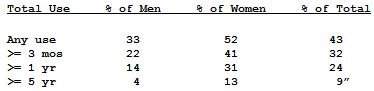

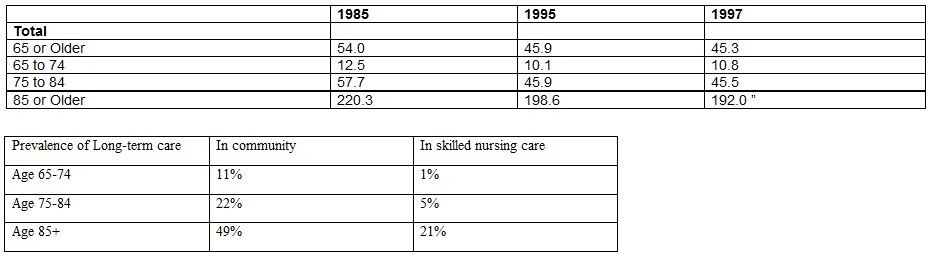

For simplification, here is the summary of the (I believe conservative) assumptions that I have used for my spreadsheet calculations: (1) 43% of 65 year olds will need and qualify for LTCI benefits, (i.e. 2 ADLs activities of daily living, like bathing eating dressing, toileting…see for example Carring.com) at some point in their lives, (2) >90% of the LTC benefit payments are for ❤ years, (3) of 65-74, 75-84 and 85+ age groups 11%, 22% and 49% receive some form of community based LTC and 1%, 5% and 21% receive skilled nursing home care.

I’ll let you be the judge of how conservative these assumptions are, by having you look at some of the sources I used to conclude that these assumptions are conservative, but also consider that:

-only 24% will spend >1 year in a nursing home

-50% of LTCI policies lapse (i.e. people stop paying for them because they can’t or are unwilling to do so)

-only 50% of LTCI policyholders entering nursing homes will receive any benefits

-65 year old will have at some point in their lives 4 years of impairment (physical and/or mental), receive 2 years of LTC at home and one year in nursing home and about half of the LTC received occurs at disability levels below threshold required for benefits. Please see the Appendix on Statistical Data and Sources at the end of this blog.

(As an aside, recently I came across a very good Canadian/Ottawa based booklet explaining what LTCI is and what are the various options associated with it (though some of the statistics as to length of stay in LTC facility in Ottawa is inconsistent with other data from the literature, specifically much longer average length stays of 3-4 years; perhaps this includes people in senior residences who are in relatively good condition (certainly not meeting 2 ADL test) but just wanting a little assistance and companionship.) You can get the report at The Council on Aging of Ottawa website and is entitled Long Term Care insurance in Canada: What is it and do I need it?)

Affordability, Need and Value

Perhaps a good way to try to look at LTCI is in terms of affordability, need and value.

First let’s consider affordability of LTCI cost. In terms of what’s the maximum you should spend on LTCI, many sources suggest the 7% ceiling (e.g. Pauline Go’s “How to save money on long term care insurance” ) but many experts warn that “the calculation should be done on the anticipated income at the time of retiring and not current (working) income”. Let’s assume “Total Income”is defined as the sum of all pensions/annuity-like sources plus 4% of assets (i.e. typically you could draw from a balanced portfolio 4%/year without seriously depleting it).You should also remember that premiums may be increased by the insurance company if they have adverse experience with a group similar to you. Now some might ask how does spending 7% of your annual income on LTCI stack up against a nice annual vacation during the 20 years of relatively active retirement years, just so that you can be more comfortable physically/financially for 2-3 years while you might be in need of LTC and/or are dying. Or, during your working years, how much of your income were you saving for your 20-30 year retirement compared to the 7% you are about to spend for LTCI? Obviously many in retirement have second thoughts on affordability (or need/value) after buying LTCI policies, since about 50% of the policies lapse before any benefits were received.

Next let’s look at the need for LTCI in terms of affordability of annual LTC cost ($25-40K in Canada depending on whether it is a public or a private source, and $45-75K in the US depending on location) and/or derived LTCI benefit for given levels of retirement income and assets. Here one must ask the question what are the reasons one is buying LTCI? The usual answers are to: (i) protect assets/income for estate/spouse, (ii) protect independence/self-reliance in case availability/cost of quality public LTC facilities deteriorates or get rationed and (iii) the rationale for many buyers and the sales pitches include a strong dose of “peace of mind” as the driver. The general rule thumb quoted by many is if assets between about $300/400K-$1.5/2.0M you might consider LTCI, below that range you might (eventually) fall back on government services and above that range self insurance might be appropriate. Actually, I suspect it a little more complex than that, as the retirees’ pension/annuity-like income streams must also have a bearing on the real or perceived need for LTCI.

Typically, a couple can live on 1.6x the spending of a single person or a single person would spend about 65% (1/1.6) of what a couple would. (This is especially true since T&E budget would likely be much lower when a spouse is in LTC).

Therefore, after one of a couple started needing LTC, one might estimate the “Additional Spending”= (LTC cost-0.35*(spending as a couple)). So, given that 92% of 3 year LTCI policyholders do not exhaust their benefits) then you might ask if you self-insured and a LTC was needed, whether you could accept asset encroachment at the level of 3-5x the annual “Additional Spending”?

If NPV represents the Net-Present-Value of the LTCI benefits received, then other metrics one might want to consider to see the likely impact of self-insurance on assets are: (1) (Max NPV)/Assets for 3/5/10 years of received benefits, remembering that >90% of LTC (nursing home) stays are ❤ years; specifically if (Max NPV)/Asset ratio <10-20% at the 3-5 years of benefit range, could you self-insure? (2) Also, if assuming 100% probability of eligibility for LTCI benefit, consider if the NPV>0 at the ages that you consider important and if yes, is it of sufficient magnitude that the loss of that NPV would encroach upon your asset beyond where you’d find it acceptable for spouse or estate.

To assess if/when we get value from an LTCI policy one might want to consider age at (or years to) breakeven (where NPV starts to move into negative territory) point (i.e. NPV=0) after starting to pay premiums for 3/5/10 years of benefits (remembering >90% of LTC stays are ❤ years); breakeven agerelative to age 85 when the likelihood of needing LTC increases significantly.

Unlike in the case of car (collision and liability) and home (fire, theft and liability) insurance where the likelihood of a loss occurrence is low but the same/similar every year, the cost of LTCI is high and the likelihood of LTC need increases with age (goes from very low to high). Since likelihood for 65 year old of needing LTC sometime during one’s life is about 43%, the insurance company pricing ends up looking more like a personal savings vehicle for the client where the breakeven point to self-insurance is (much) less than or equal to the age when the probability of needing LTC starts increasing (80s). This combined with the required reduction of lifestyle throughout the hopefully relatively long, active and healthy retirement years to pay significant LTCI premiums so benefits may be received for the likely short incapacitated period is a hard trade-off to make even for people in their 60s (never mind for those in their 40s even if premiums are much more reasonable, but LTCI is not top of mind and you are still likely paying your mortgage and for your children’s education).

Such NPV calculations, even if input assumptions are uncertain, might be a good way of comparing different LTCI policies.

Specific examples

4% discount rate for NPV calculations implicitly assume perhaps 2-2.5% inflation rate in general (CPI). The 5% compound inflation protection of benefits, when included, is to protect against much higher than CPI level increases in LTC-cost observed historically.

If cost of LTCI is defined by the forgone investment value if premiums were instead invested at 6% (or 8% or 10%) return, then NPV is the discounted “Net Benefit”= LTCI Benefit-LTCI Cost, where LTCI benefit is the discounted value of the 3, 5 and 10 year benefits considered.

The decision to buy or not will no doubt still will be subjective for many people. But for those who want a better understanding of the value they might expect to get for their money, let’s drill down a little more quantitatively to determine if an LTCI policy is good value or not. Putting aside the “peace of mind” argument and sales pitch induced fear associated with LTC cost, the bottom line for LTCI is still asset protection for the next generation or for the spouse not requiring LTC first. So what are we buying for all the premiums that we sign up for and the potential increase(s) of those premiums that are outside our control? And always remember that “computing is for insight not numbers”, especially when we are dealing with perhaps somewhat uncertain models.

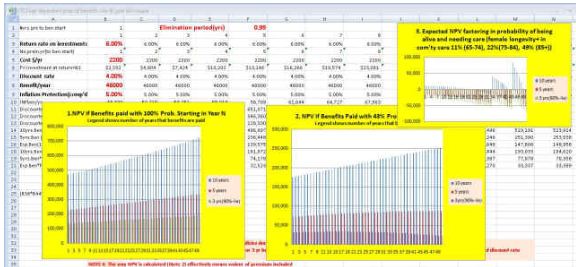

So let’s see where is the expected value in these examples? The graphs below show the NPV of the benefits starting 1-50 years after buying the LTCI. In each example there are three graphs. Graph #1 shows the actual NPV value when one actually (needs and) receives LTCI benefits (i.e. assumes 100% probability of getting benefits) and graph #2 the expected NPV, i.e. corrected for the 43% age-independent probability of receiving LTCI benefits. The three bar charts are NPV values when benefits are received for 3, 5 and 10 years, respectively. So given that 92% of those with 3 year benefit coverage don’t exhaust coverage, we won’t be much in error assuming that 3 years of LTCI benefit payments is the 90 percentile point for benefit duration. The average/median benefit duration is pessimistically 1.5-2.5 years (<3 years) given that even if LTC is required for longer one may not qualify immediately and it is common to have 90+ day elimination period. Graph #3 in each example also includes in the calculation the longevity expectation (calculation used female longevity statistics generating more optimistic expected NPV for males) of a 65 year old to the assumed start of benefit age and a very pessimistic assumption of benefits being paid between ages 65-74, 75-84 and 85+ with 11%, 22% and 49% probability, respectively. These probabilities are not for LTCI benefits, but for “in community” LTC and are significantly higher than even the “in skilled nursing care” need probabilities of 1%, 5% and 21% which are more likely to be the statistics for those actually eligible for LTCI benefits).

Example 1-If you are a couple aged 69/65 years old male/female, are you prepared to spend about $4200/ year each for 20 years to receive (in Canada) an un-indexed reimbursement (not disability, i.e. not only must you meet benefit triggers, but you also get paid only for qualified receipted expenses) policy with 90-day elimination period and $36,000/year lifetime benefit should you need it and IF you ever qualify for it (typically two ADLs). Perhaps we can get a handle on this by looking at “affordability need and value” for this example.

Using the rule of thumb that people may spend typically 4% and certainly not more than 7% of their annual income (remember income is pension-like income streams plus 4% of assets) on LTCI premium then if both husband and wife would buy coverage the cost would be about $8,400/year requiring an income range of $120,000-$210,000. To buy coverage for one of them would require $60-$105,000; if LTCI was bought only for one, which one would you insure (the female would likely need it later but for longer) and would it buy you the “peace of mind” you crave for. The point here is that you will have to continue paying this premium for 20 years in this case (or life in some others) and as the cost of living in retirement is increasing over time, the ability/willingness to pay for the policy will decrease especially with the decreasing real value of the un-indexed benefit. There is also the risk that premiums will increase over time (as permitted by most policy T & Cs). For Canadians, assuming $35K/year LTC cost, for people with incomes/spending greater than 100K/year, they might self insure for $36K/year benefit, since when their non-LTC spending would drop as well; taxes would likely be lower as well as some/most of the LTC costs may be tax deductible. But would a 65 year old retiree couple whose pre-tax income is $60K and after tax income may be <$50K be prepared to spend $4,200/mo for a $36,000/year benefit policy? I guess it’s a matter of temperament, to forgo almost 10% of after-tax income while healthy to protect income while one of the couple is sick? And you might really have to spend twice that much to cover both!

If the objective is asset protection (for spouse/partner or estate), is there sufficient asset protection provided by LTCI purchase. A $4,200 annual premium for 20 years using a discount rate of 4%, results in the NPV of premiums to be <$60K. (As an aside, compare value to you of this $36K/year LTCI to the >$50K/yr longevity insurance income starting at 85 that a premium of $60K would buy at age 65; average LTCI benefit duration is about 2 years whereas average life expectancy for an 85 year old is about 5-6 years.) Note that the 43% probability of needing nursing home care (though average time of use is about 2 years of which only half is at disability level qualifying for LTCI benefits) is similar to the probability of about 50% of collecting longevity insurance given that for a 65 year old the unisex life expectancy is just under 85.)

The breakeven point (where NPV=0 and starts to move into negative territory) for those who assume that they are certain to require/receive benefits for 3 years (about 90%) is 13 years, while the expected breakeven for the entire population (with 43% age-independent uniform probability of getting benefits) of LTCI buyers is 7 years! For the few percent that bought and need longer (>3 years) benefits the NPV is higher. The highest NPV is when benefits are required immediately after buying the policy; those having/requiring 3,5 and 10 years of benefit staring immediately after purchase have NPV of $80K, $150K and $270K. However, the expected breakeven for the entire population of purchasers is 7, 11 and 17 years (or ages 72, 76 and 82) for those requiring 3, 5 and 10 benefits; the maximum NPV is correspondingly $33K, $52K and $105K, as shown below.

As for Graph #3 in the above example, even at the very pessimistic assumptions of probability of need (or very optimistic assumptions of receiving benefits), has NPV<0 for just about all ages. Recall that Graph #3 uses still very highly optimistic but age-dependent probabilities for LTCI benefits.

So the question you must ask is “How much asset protection is a person getting in this policy?” And, don’t forget that you really need coverage for both spouses to get “full” protection. Would somebody with $1M-1.5M of assets want to spend $4200/year to get an expected maximum (and rapidly diminishing) NPV of $33K, 52K and 105K for 3/5/10 years of benefits, assuming benefits start during the first year the policy is in force (a very low probability event). How about at $750K of assets? How about $500K or less and could they afford it without significantly affecting their lifestyle? Again, if person/couple has no assets or expects to deplete assets during retirement, then government ultimately pays for nursing home- in this case the need to buy LTCI is even more elusive.

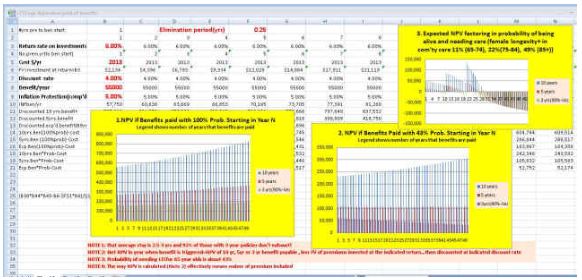

Example 2- Next is a more interesting case reported by Jeff Opdykewho purchased for $2,200 a $125/day ($45,625/year), one year elimination period policy with 5% compound indexed benefit for a 42 year old couple (usable by either or both) with coverage as long as care is required. So let’s see what the NPV graphs look like in this case?

If you are a conservative investor (assuming 6% forgone return on premiums, shown in the next set of graphs below) this looks like great deal, when compared to the previous example. (In fact, the probability of one of a couple receiving LTCI benefits is somewhat greater than that for an individual, so leaving the probabilities unchanged will somewhat understate the NPV associated with this policy, even though maximum annual benefits are unchanged.) Expected NPV is positive for 3/5/10 years of benefits received anytime in the next 50 years for 100% (graph #1 below) and 43% (graph #2 below) probability of receiving benefits. Graph #3 also shows that the included 5% compound inflation gives catastrophic lifetime (40-50 year span) coverage if needed, with NPV>0 even if 10 years of total benefit starts for the couple as late as age 90.

This policy is for a relatively young couple (age 42) and likelihood of needing LTC is probably in 40-50 years, so it’s worth looking at the impact of more aggressive investment return assumptions. For a more aggressive investor (assuming 8% forgone return on premiums) the NPV>0 for all ages/cases when probability of receiving benefits is 100% (graph#1). For 43% age-independent probability of receiving benefits the NPV goes negative NPV<0 at age 72 for 3 years of benefits and at age 92 for 5 years of benefits. (I assume this was a disability, rather than reimbursement, benefit policy with 2 ADLs of 6 as the threshold. Depending on one’s level of risk tolerance and need for “peace of mind” this may still be acceptable value, as it was for a financially knowledgeable and savvy individual like Opdyke; remember that by insuring at age 42 one is protected against rare but catastrophic event of a truly long need for care in case of a debilitating accident or stroke.)

For what it’s worth, I looked at published quotes for various LTCI situations from many sources and this was the best case where the numbers (together with “peace of mind”) may lead me to seriously consider an LTCI policy especially if it was from a very highly rated company (here it was) and there was premium cap (there wasn’t). One could consider this policy providing catastrophic coverage not just to the extent that it has a one year elimination period, but also because both individuals are covered with 5% inflation adjustment for an indefinite period of required/qualified LTC.

Example 3- Let’s consider another U.S. based example for a 65 year old LTCI buyer, the last column (U.S. 2008 example) from the Table in LTCI Overview blog. This is a 5% compound indexed portfolio paying a maximum of $55K/year for 3 years with a 90 day elimination period; the premium is $2013/year for a 65 year old. Notice that forgoing the value of the invested premiums at 6% return, still shows NPV>0 for all ages at 100% and 43% uniform probability (graphs #1 and #2 below). The maximum NPV is about $165K if benefits would start during the first year of the policy and continue for the full 3 years; recall this policy provides a maximum 3 years of benefits, so the 5 and 10 year curves in the following picture are not relevant. Even graph #3 the 3 year NPV>-$20K all the way to age 92. So this is also much more favourable than Example 1.

Conclusions

So I am still struggling to find a compelling example of when one must have the LTCI coverage. Perhaps the case of a very high pension income (compared to spending level) fully indexed is associated with relatively low level of assets which one wants to protect under all circumstances and/or one might have a higher estimated expected probability of qualifying for LTCI, then one might have a convincing case.

The other point perhaps is that I am not sure if the conclusion from the above examples is that U.S. policies seem to be more attractively priced than Canadian ones, or that 5% compound inflation protected portfolios are better value than those which have no inflation protection (or perhaps a little of both). In any case, inflation protected policies are the only ones worth considering, unless your expectation is that you’ll qualify for LTCI benefits very early in the life of the policy.

If you still think that your “peace of mind” demands that you buy an LTCI, then consider:

-a joint policy for an annual/total dollars usable by either

-compound inflation protection (5%), especially for younger (age <70) buyers

-longer elimination periods 0.5-1.0 years to lower premium

-benefit triggers: 2 ADLs out of 6, or cognitive impairment

-highest rated company, to increase the chance that it will be around to pay in 20-40 years

-waiver of premium (i.e. premiums stop when benefits start and/or only 15-20 years of premiums)

-capped premium levels

-non-forfeiture of policy if you stopped premiums (recall that 50% of policies lapse); perhaps automatically convert to “paid up” status

-prefer disability rather than reimbursement benefits (i.e. if hurdle met you get specified $/mo)

–combination products: life insurance or annuity combined with LTCI; perhaps ask your insurance company if they have LTCI riders to be added to these type of policies that you may already have

Or, you may get sufficient peace of mind if you put aside and invested each year the equivalent of the premiums (7% of “Total Income” during retirement) and created a personal LTC-fund that you could draw on should LTC be required; if not required then it becomes part of your estate.

P.S. As to those who already have LTCI policies, you are not home free. Here is a September 2009 article in the Sun-Sentinel entitled “Make sure your long-term-care insurer pays up” to see the challenges one might have to deal with when it is time to get benefits (especially from a reimbursement type policy).

Appendix: Statistical Data and Sources

David Braze in his ”Those dratted statistics made easier” at Fool.com reports that “While estimates vary, one source places the lifetimerisk of institutionalization for those reaching age 65 in 1990 at 43 percent — 52 percent for women and 33 percent for men (Kemper and Murtaugh, 1991). However, research has shown that most nursing home admissions are of relatively short duration — three of four are for less than one year (Liu et al., 1991).”

Furthermore, the Kemper and Murtaugh study indicates that “that 37% of those age 65 or older at death had spent some time in a nursing home during life. Using that data, the authors then projected nursing home use for those who reached age 65 in 1990 as shown in this table:

In another Fool.com article by David Braze “Should you buy long-term care insurance?”He quotes from Joseph Mathews’ book “Long Term-Care: How to Plan and Pay for It”: (i) Roughly 50 percent of all policies lapsed before any benefits were paid, (ii) About half of policyholders who entered a nursing home never received a benefit from their policy, (iii) When benefits were paid, they were far less than the actual cost of care.

The Robert Wood Johnson Foundation’s study between the years 2002-2007 entitled “What disability and Long-Term-Care Risk do retirees face”their key findings include the following points: (i) People turning 65 face, on average, four years of chronic physical or cognitive impairment during their remaining lives, nearly two years of long-term care at home and one year in a nursing home, (ii) On average, slightly more than half of long-term care received by retirees occurs at disability levels below commonly used functional thresholds for receipt of insurance benefits.

Hawbaker and Goeller’s “Long-Term Care”Risk Management Workshop

“Only 4.5% of those over 65 reside in a nursing home facility.

-2/3 of all men over age 65 and 1/3 of all women over age 65 will never stay a single day in a nursing home facility

-Over 50% of all nursing home facility stays will last less than 6 months

-Only 25% of all women over age 65 and 10% of all men over age 65 will stay more than one year in the nursing home facility

-Only 10% of those over 65 will stay more than 3 years in a nursing home facility

-The average length of stay in a nursing home facility is between 18 and 20 Months”

In Financing Long Term Care’s “Long term care risk”

“Some estimate that the actual risk of needing long term care (either in the home or in a nursing home) is 50%. This risk is significantly greater that the risk associated with other life events. For example, insurance professionals (Kesy, 2000) cite the following probabilities for other life events: (i) Probability of losing a home to a fire is 1 in 1,200, (ii) Probability of having a car accident is 1 in 240, (iii) Probability of a hospital stay costing $30,000 is 1 in 15.

In 1997, the total rate of nursing home residence for persons age 65 and older was 45.3 per 1,000 (Federal Interagency Forum on Aging-Related Statistics, 2000, p. 92). The following table breaks down rate of nursing home residence among persons by age group. It is important to note that rates of nursing home use increase significantly with age:”

According to “Long-term-care insurance for less” in December 2008 issue of Kiplinger, with Genworth’s non-traditional Cornerstone policy (which excludes room and board, has a 20% co-payment) the average claim is 2.5 years, while a survey of insurers indicated that “92% of buyers who have three-year benefit periods and eventually file a claim do not exhaust their benefits. Earlier Kemper and Murtaugh’s 1991 study length of stay studies “reported average stays of 19 months for males and 26 months for females”.

Other interesting statistics for your consideration are available at the Family Caregiver Alliance.