A couple of months ago a reader asked what I thought about LTCIs. Not being well versed on the subject I started reading about them and the more I read, the more it became obvious why people are so confused about what to do about LTCI. My conclusion: I am not ready to suggest that you run out to buy, but I want to think more about the subject. Please consider this an introductory blog on LTCIs. I plan to follow it up with at least one more which will discuss LTCI a little more quantitatively.

In a nutshell

Having an insurance company pay for our long-term care costs that (according to assorted published data) about 40-50% of us will need at some point during our lives certainly sounds very attractive for our peace of mind. However, would you buy an insurance where:

-Premiums: (i) are expensive (50% load factors- i.e. for each $1 of premiums collected only $0.50 is paid out in benefits), and (ii) yet you don’t know how much more expensive they’ll get before you collect any benefits

-Benefits: should you be among those who need long-term care, you are not sure if and when you might qualify, or even how much of the long-term care cost will be covered

-Complexity: LTCI policies are not standardized; they are difficult to understand and may be open to interpretation by the insurance company which wrote the policy and possesses asymmetric information

Why people consider buying LTC insurance? – What is being insured?

-Reduce chance of exhausting or severely depleting assets for retirees and the next generation. Examples include : (1) in case of a couple, protecting assets for spouse not requiring LTC first (consider the low probability-high impact scenario of 70 year old spouse with a stroke or Alzheimer may require 5-10 years of facility based LTC ,while the other spouse may continue to have most of the previous expenses of living at home; such a scenario could radically deplete the assets available for the un-institutionalized spouse and essentially impoverish him/her by the time that (s)he is 80 years old), and/or (2) protect estate for the next generation. The first of these two reasons would be my driver for LTCI, i.e. to prevent other spouse from impoverishment.

-Getting a stroke or Alzheimer or becoming incapacitated as a result of an accident in one’s 50s could result in truly long duration LTC expenses

– Having some control/options on the quality and quantity of long-term care (access to higher priced or additional services) rather than having to accept that which may be offered by the government

– Cover some part of the cost of long-term care (depending on plan, may cover some/all of home-care, assisted living and/or nursing home care)

-You don’t want to be a burden on your children financially or have conflict with them over “the level (too little or too much) of LTC spending”; e.g. being financially capable and in control to make the LTC spending decision rather than rely on family

-For most retirees LTCI may be a better place to spend insurance dollars than life-disability-critical illness insurance, which may not be necessary for many

Who is LTC insurance appropriate/applicable for?

The most commonly quoted candidates for whom LTCI is applicable are those who have assets within the range of $300K-$2M. For those with assets <$300K there is significant risk that they won’t be willing or able to continue paying the premiums over the long term and they may rely on government (‘welfare’ equivalent) once they exhaust their assets. At the other end of the range $2M is mentioned as the asset base beyond which self insurance may be more appropriate. For example Opdyke “The policies are generally most appropriate for people who have between $500,000 and a couple million dollars in net assets, and who want to protect some of that money for heirs, since an LTC policy will cover costs that otherwise might eat up those savings”. Similar ranges are quoted in many other sources that you’ll come across.

The potential problems with LTCI

-It is too expensive- “the typical policy purchased exhibits premiums marked up substantially above expected benefits. It also provides very limited coverage relative to the total expenditure risk” according to Brown and Finkelstein 2007 (The load on policies is about 50% for LTCI, when factoring in the effect of those who stop paying premiums and forfeit future benefits, compared to 5-25% on most other forms of insurance; on male policies the load is especially onerous with unisex rates according to these researchers. Load of 25% means that the buyer will on average, get back only 75 cents in expected present discounted value benefits for every dollar paid in expected present discounted value premiums! In LTCI case then, a load of 50% means that on the average buyers get $0.50 of benefits for each $1.00 spent on premiums; and remember that this is based on U.S. data- it is not unusual for Canadian life insurance company product premiums to be higher and effective loads to be higher.)

-Insurance companies have the right, and they often do increase rates (based on experience with a whole class of insured similar to you, though not specifically as a result of your unique experience). As a result, will you choose or be forced to discontinue premium payments and lose coverage and the paid premiums? Will you have the assets or the income necessary to continue paying for the policy? Is there a maximum cap on the premium that you’ll have to pay?

-Will you have difficulty qualifying for benefits when you need them? What are the benefit triggers specified in the policy? ADLs (activities of daily living) and/or cognitive impairment are often used as benefit triggers. It is better to have a policy specifying 2 ADLs rather than 3 or 4 ADLs from a list(which includes bathing, dressing, eating, walking, etc); avoid “medically necessary due to illness or injury” clause and “prior hospitalization stay” requirement ,and avoid exclusions of Alzheimer, heart disease, diabetes, cancer (see an excellent reference at Carring.com ). It is certainly possible, especially for a single retiree without a spouse/partner or family able to provide care, that the individual (or the family) may decide that additional care is required at home or at an assisted-living facility well before that individual meets her LTCI benefit triggers; so one could be paying for long-term care for years before qualifying for benefits under their plan.

-Will the insurance company be around in 20, 30 or 40 years to pay out (check out credit rating of insurance company ( A.M Best has U.S and Canadian insurance company ratings accessible for free by simply registering at their website, Moody’s , Standard and Poor’sand Weiss also rate insurance companies; check state/provincial maximum guarantees, if any, in case of insurance company can’t pay)

-Only part of the total LTC costs may be covered due to inflation erosion and/or annual $ maximum and/or cap on total number of years. Brown and Finkelstein “estimate that the typical policy purchased by a 65-year old and held until death covers only about one-third of the expected present discounted value of long-term care expenditures”.

-There are no standards for LTCI policies. LTCI contracts are very complex and their language often is very difficult to understand. After paying premiums for decades it is too late to find out, when care is required, that insurance company’s interpretation is less comprehensive or that benefit triggers present a higher hurdle than you expected. So thorough understanding of benefit triggers, inclusions, exclusions, costs and assorted other policy fine print are critical. LTCI policies are a major investment, so don’t buy it if you don’t fully understand it.

-Make sure that your policy is guaranteed renewable. Recently an insurer in Pennsylvania dumped LTC policies into an independent trust, likely because they found them not to be profitable (enough), thus exposing the insured to reduced benefits and/or increased cost (see WSJ Insurer Casts off Long-term care policies )

LTC Costs

-The primary cost structure difference between LTC in U.S. and Canada is that: in Canada (e.g. Ontario ) the government provides funds to nursing homes directly, however there is a specified co-payment required from the user (about $18K-$24K per year), in the U.S. average costs are quoted in the $60K-70K range and under some circumstances Medicare/Medigap/Medicaid may cover some of the cost (see Cost of Care/Who Pays ). In both countries, individuals without assets would be entitled to care at some level in exchange of the government pension like Social Security or CPP/AOS).

-Canadian costs: “For example, a nursing home in Ontario, regardless of ownership, costs residents $1,544 per month for a basic room, $1,787 for a semi-private room and $2,091 for a private room. Home care, which provides assistance such as visiting nurses, help with bathing and meal delivery, generally costs $15 to $25 per hour for homemaking and personal care and $25 to $65 for nursing care, according to insurer Sun Life Financial” in Planning for the inevitable: A wake-up call for long-term care planning.

–Manu Life’s Canadian website reports detailed 2008 province-by-province costs for nursing homes, residences and home care. For example in Ontario some private seniors’ residences have a portion of the facility allocated to those who are “functionally dependent” and they quote a price range from $2,500-$6,000 per month. Hourly cost of private home care services are reported to be about $20, with skilled nursing services between $30-60/hour.

-McNaughton in “Long term care insurance in Canada” argues that we should be planning LTC expenses based on private rates due to the long and growing wait times to be admitted, the deteriorating quality of care, the reduced flexibility in selecting location.

-U.S. costs: “The average private room in a nursing home costs $213 a day, according to the MetLife Mature Market Institute (rates top out at $352 a day in New York City). The average daily cost in Kansas City…. is $140.” (Kiplinger December 2008 )

-At Genworth the average claim is 2.5 years, while a survey of insurers indicated that “92% of buyers who have three-year benefit periods and eventually file a claim do not exhaust their benefits”. (Kiplinger December 2008). Earlier Kemper and Murtaugh’s 1991 study length of stay studies “reported average stays of 19 months for males and 26 months for females”.

-Note however that “most LTC policies now insure the holder only up to certain daily dollar expenditure (as opposed to medical coverage that may insure all reasonable and usual charges), it might be said that LTC insurance does not necessarily provide insurance against catastrophic loss. Rather, it offers a defined payment much like life insurance…” (Gold, VanderLinden and Herald “The Financial Desirability of Long-Term Care Insurance Versus Self-Insurance” )

LTCI Cost

-Unlike in other types of insurance, there are no standardized LTCI policies. So it is difficult to readily comparison shop for LTCI. Generally, policies are subject to premium increases based on group experience or even transfer to a “government pool” with lower benefits and/or higher costs (as mentioned above).

-LTCI cost is a function of age, health (in case of poor health your costs will be higher or they may exclude current illness or you may not even be eligible to purchase LTCI), maximum number of years of coverage (1, 2, 3, 4, 5 years or in some cases as long as needed) or maximum dollars covered, elimination period (30, 60, 90 days are typical), maximum amount of coverage per day or year, whether you are male or female (female LTC stays are longer), married or single (couples tend to take care of each other and therefore require less care) and of course also dependent on what’s covered/excluded and how high is the hurdle to start qualifying for benefits; waiver of premium (i.e. no premium payable when benefits are received) also may be included.

-Premiums are lower when buying LTCI at a relatively young age; this also eliminates the risk that you won’t qualify to buy later on due to health problems. Of course the insurance company must be around in 40-50 years to pay benefits, policy benefits must have adequate inflation protection (the ravages of inflation when policy bought at ages 40-50 can render the benefits worthless at ages 80-90), yet you would have paid premiums and be exposed to premium increases over a longer period of time.

-Additional riders (options) available: inflation protection (which comes in various forms simple/fixed-dollar or compound adjustment, amount of adjustment may be a specified fixed percentage- 2%, 3% or 5% or changing with CPI. You must also keep in mind that U.S. nursing-home prices are reported to be growing at 6% per year. Look out for: limits on maximum number of years/age/caps associated with inflation adjustments), inclusion of home-care and/or assisted living (in addition to nursing home coverage) with/without constraints on source/certification of the hired help, flat monthly payment independent of actual expenses, premium waiver once LTCI benefits start.

-In Canada premiums are not tax deductible; benefits are not taxable, though some LTC costs paid may be tax deductible. In the U.S., ‘Qualified’ LTCI policy premiums may be tax deductible to some extent (you can read about tax qualified and non-tax qualified policies at Wikipedia ; the maximum eligible amount appears is a function of age, the taxpayer must file an itemized return and the amount deductible to the extent that when it is “added to other unreimbursed medical expenses, exceeds 7.5% of the taxpayer’s adjusted gross income” read(You better check with your tax advisor). There may be tax advantages for an owner of a private business to acquire LTCI through the company. (Check with your accountant.)

-The Canadian focused Employee Benefit News has an LTCI checklist that you may want to look at

-Canadian sample price can be viewed at Sun Life

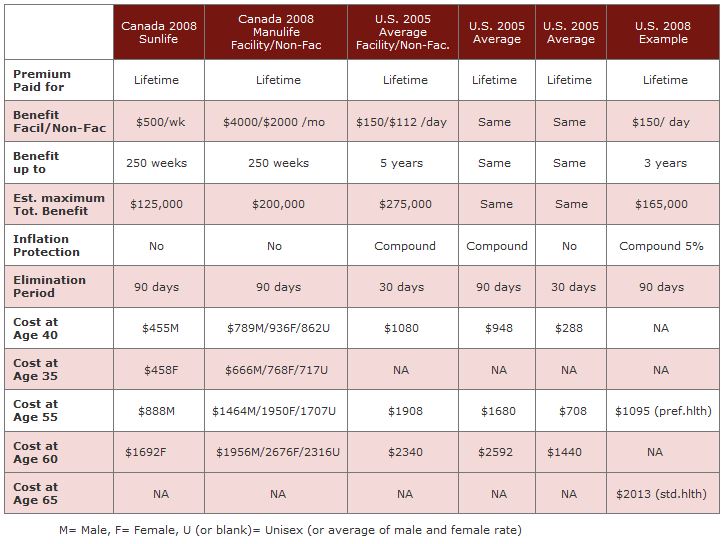

-A recent Employee Benefit News article by Carolyn Hirschman indicates “For example, Manulife Financial policyholders select a total amount of coverage ($25,000 to $2 million) and a percentage of that amount to be paid monthly when long-term care is needed (0.25% to 2%). It appears that you contract for a percentage of that maximum say 0.5%, 1% or 2% that would be payable monthly when non-facility based LTC is required; when facility based care is required the monthly amount is doubled but the total maximum is unchanged. Manulife LTCI buyers also have an option to pay a higher monthly premium for 15 years rather than lifetime premiums. Manulife’s Canadian websitehas lots of valuable information.

-U.S. rates (based on 2010 data from MetLife) quoted at the National Clearinghouse for Long-Term Care Information indicate an annual premium of about $2000 (there are indications that prices are higher since 2005) for a 5 year max $150/day facility care $112 (75%) home care (lifetime $275,000) with 30 day elimination period and compound inflation protection (not clear if related to general or LTC related inflation rate). The website also provides some prices for a policy with somewhat different input parameters; so for example 90 rather than 30 day elimination period would be about 13% cheaper, 3 year vs. 5 year coverage is about 18% cheaper, no inflation protection for a 65 year old would be about 50% cheaper than 5% compounded protection.

-In Things to Consider (pp.15-16) there is an explanation of the different benefit payment methods that you must pay attention to when you purchase the policy. A $150/day benefit will mean different actual payment to you, depending on whether you have: reimbursement (100% of expenses are reimbursed up to some pre-set amount), indemnity (pays a pre-set amount on any day that you have LTC expenses, irrespective of the amount of those expenses) or disability (pays a pre-set amount for any day that you are disabled, even if you have no expenses) policy.

-As you read LTCI literature you frequently come across the warning that you shouldn’t spend more than 7% of your income on LTCI. You must also remember that even if this rule of thumb is valid, it can be misleading, because you usually are paying premiums for life and certainly through much of retirement, therefore you better apply that to your retirement income and fact in the potential premium increases.

So you must read the policy very carefully! I tried to summarize the Canadian and U.S. data in a single table below, but since the data is from different sources and not necessarily identical parameters (though I tried to keep them close), they are not a perfect apples-to-apples comparison, it is just a simplest mechanism to present some of the available options in Canada and the U.S. (e.g. Sunlife has three types of plans reinbursing: eligible expenses on a given day up to a maximum, fixed daily amount if you have eligible expenses that day, income when care is required without proof that expenses were incurred-reimbursement, indemnity and disability- and I couldn’t determine which was the priced policy.)

-Another interesting data point is Jeff Opdyke’s 2006 policy with a long elimination period: $2200/year for a 42 year old couple for $125/day for unlimited number of years rising at 5%/year, with a one year elimination period

-in Long-term care insurance for less (Kiplinger December 2008)

quotes $4,000 a year premium for a 55 year old “fully loaded policy with lifetime benefits, a 5% annual increase in benefits and a waiting period of 60 to 90 days” (Note the differences from the $2,000 policy in 2005, mentioned above, are “fully loaded”, “lifetime benefits”). Kiplinger then talks about the following two lower cost options that have become recently available.

-John Hancock’s Leading Edge joint LTC policy (for a couple 55 and 57) cost 1,700/year for a 5 year $100/day with CPI (not necessarily 5%/year) inflation increased benefits for each, but all 10 years of available benefits are usable by one of the spouses in case of a chronic illness (This protection model feels right, if you tend to believe that the purpose of LTCI is asset protection to protect the lifestyle of the spouse who is second to require or may not end up needing LTC.)

-Genworth’s Cornerstone policy “does not cover room and board for assisted living, only the custodial services”. “55-year-old would pay about $1,000 per year for a Cornerstone policy with a $275,000 pool, $150 daily maximum benefit, 90-day waiting period, and a 5% inflation factor.”

Other approaches to covering long-term care expenses

-If assets <$200K it is often suggested that LTCI is not appropriate because it is not affordable and likely will exhaust assets and become reliant on government assistance or if assets >$2M one is presumed to have sufficient assets to self-insure)

-If pension-like income is indexed (and from a guaranteed government source) and higher than LTC cost, then it may be sufficient to cover LTC expenses for a single person, for a high income couple with no assets LTCI may be a sensible source of protection

-Consider insuring the wife and not the husband, given the often unfavorable LTCI pricing for males (e.g. unisex pricing even though average LTC stay for males is much shorter)

-If you have sufficient assets and you have a plan for an estate by spending no more than 4% of your assets from a 50:50 stock bond portfolio, then if necessary you can dip into the estate to pay for LTC (e.g. why not stress test your self-insured retirement plan by including 3-5 years of $50K-$70K/year inflation adjusted LTC expenses and test scenarios with LTC starting at age 75, 80 and 85.) Another way to look at self-insurance is to ask yourself how much of your assets could you (or would you be prepared to) put aside to pay for LTC (for you or your spouse), and could you still maintain your current/desired lifestyle.

New approaches/Other factors

-For the small percentage of those who end up with chronic condition that require in excess of three years of care, Kiplinger December 2008 reports that “about 25 states offer, or will soon offer, partnership programs that let you apply for Medicaid without turning yourself into a pauper once you run out of LTC insurance benefits. The rules are complicated and vary by state, but the principle is this: If your insurance pays a total of $200,000, for example, you can shelter $200,000 of assets from Medicaid above and beyond what the law allows.”

-Annuities combined with LTC benefits (essentially larger annuity payments once LTC is needed) “Applying financial engineering to wealth management”

-Life insurance convertible to LTCI

-Some companies started to offer reduced benefits if you can’t continue to pay for (increased) premiums at some point prior to needing benefits

-Catastrophic coverage- long elimination periods vs. short elimination period. There are two schools of thought. There are those who argue that while premiums may be lower with a 1-2 year elimination period many/most of the people, even among those who will end up needing LTC, will end up not collecting (m)any benefits. Then there are those who argue that people opting for short elimination period and say 3-5 year coverage end up paying much higher premiums and are still exposed to only partial coverage of expenses and bear the risk of longer LTC stays. (My inclination as a general rule when I buy insurance, is to insure risks that I can’t afford to or don’t make sense to take; so right now if I did decide to buy LTCI, I would lean toward longer elimination period.)

-I have come across references to policies requiring a finite number of payments, but have not come across any references to a single lump sum payment (which would prevent future price increases)

-You may have access to group policies (employer, professional organizations, affinity groups), but make sure you understand the advantages as compared to other options

Some key providers

Caring.com suggests three sources where you can start looking for LTCI policies: insurance agents, your (larger) employers and professional/affinity groups.

U.S.: ManuLife/Hancock, Northwestern Mutual Life, Genworth, MetLife, Mass Mutual Lincoln Financial

Canada: SunLife , Manu Life, Great West Life, Canada Life

LTCI Calculators

SmartMoney LTCI CalculatorLTC insurance evaluators (It appears that the probability of needing LTC and tax impacts are not included)

CalcXML LTCI Calculator

Resources

Family Caregiver Alliance (U.S. state-by-state resources)

Summary

As I indicated at the start, please consider this an introductory blog on the LTCI. I plan a follow-up looking at the available data in a little more quantitative way, based on some of the more technical references included below, but not discussed.

This is complex and confusing, and a lot of purchases are no doubt made out of fear. After reading about LTCI for a couple of weeks, I am yet to be persuaded that this is something that I must recommend that you rush out to buy today, in its most common incarnation. I have not dismissed it completely; I am just not persuaded as yet. Ultimately this is a personal decision, that should be based on a full understanding on what you are buying and why do you need it.

I hope you found this blog useful. I certainly found it educational to research it. Next blog on this subject will cover the value of LTCI by looking at the numbers (net present value of cost and benefit, probability of occurrence, when/how to self insure, etc)

References (in no particular order)

Opdykebought one year elimination period

Caring.com(one of the best)

U.S. Government’s National Clearinghouse for LTC information

MSN Money’s take on LTCI

“Avoiding Fraud When Buying Long-Term Care insurance”

“Applying financial engineering to wealth management”

“Long-term care health coverage a hidden casualty of economic slide”Kaplan

“The Financial Desirability of Long-Term Care Insurance Versus Self-Insurance”FPA Journal- The Financial desirability of long-term care

Long-term care insurance for less (Kiplinger)

Consumer protection and long-term care insurance: Predictability of premiums

Do you mind if I quote a couple of your posts as

long as I provide credit and sources back to your website?

My website is in the exact same niche as yours and my visitors would

truly benefit from some of the information you present here.

Please let me know if this alright with you. Many thanks!

Generally yes…see Legal tab of the website at https://retirementaction.com/legal/

Thanks for your interest…peter