Risk perspectives: What is risk? Its measurement, dimensions, modeling (asset classes, risk factors and regimes)

In a nutshell

After getting walloped twice in a decade with massive market crashes, suddenly everybody is interested in the subject of risk. You’ll find below a collection of perspectives on risk: what it is and attempts at measuring and modeling risk, so we can ultimately try to manage it. What this blog discusses are the challenges associated with defining measuring and modeling risk. (This is not intended to be a definitive work on risk, rather just view of the considerations and difficulties associated with the topic. In a follow-on blog, we’ll try to look at some basic risk management techniques.)

What is risk?

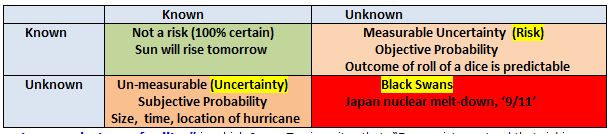

Frank Knight in his 1921 book “Risk, Uncertainty and Profit” writes that to preserve the difference between a “measurable uncertainty and an un-measurable one we may use the term “risk” to designate the former and the term “uncertainty” for the latter….We can also employ the terms “objective” and “subjective” probability to designate to designate the risk and uncertainty respectively…the practical difference between the two categories, risk and uncertainty, is that in the former the distribution of the outcome in a group of instances is known (either through calculation a priori or from statistics of past experience), while in the case of uncertainty this is not true, the reason being in general that it is impossible to form a group of instances, because the situation dealt with is in a high degree unique.” So, objective probability (risk) might be the probability of getting a head in a coin flip, while subjective probability (uncertainty) might be the probability, predicted in April 2011, of getting a Category 3 or higher hurricane in Miami during the June-November 2011 hurrica

Risk, uncertainty and Black Swans

The simplest and perhaps the most meaningful definition of financial risk might be “the probability of not being able to meet your objectives” (e.g. your monthly expenses, or retire at your planned age in your planned lifestyle, etc). So financial risk is not some measure of what the market will do, but the impact of what the market will do on your objectives.

Yet one of the most common definitions of market risk is volatility (standard deviation if return can be represented by a normal distribution – or Bell curve), which happens to be a measure of risk (see below). This is also happens to be one of the least meaningful definitions of risk to the average investor.

Another definition of risk is mentioned in a recent WSJ article discussing risk entitled “How now, 36,000 Dow? The ominous undertone of rallies” in which Jason Zweig writes that: “Economists contend that riskier assets must offer higher returns, or no one would invest in them. That is a fallacy, says Howard Marks, chairman of Oaktree Capital…Riskier assets don’t necessarily offer higher returns, Mr. Marks says; they only appear to do so. “It’s really simple,” he says. “If risky investments could be counted on for higher returns, then they wouldn’t be risky. And if investments weren’t risky, then they probably wouldn’t appear to promise higher returns.”… But by Mr. Marks’s common-sense definition of risk—”the likelihood of losing money”—rising prices are pure investment poison. The higher and faster prices go up, the farther and harder they have to fall… Meanwhile, cash is moving out of municipal bonds and emerging-markets stocks as their prices fall. If that keeps up, they will get less risky, not more—and more attractive, not less.”

And then an allegorical description of risk as told by Kenneth French, of Fama and French fame, by means of a story about travelling to NYC. You have the choice a long, winding, smooth but slow road which gets you the in a long time, or you can take a short and bumpy road which is full of pot-holes which could get you there much more quickly. Then risk means that you not only have to live with the rough ride of the bumpy road, but also with the possibility that your car might break down in one of those pot-holes and you’ll never get to NYC!

Measures of risk?

The most commonly used definition of portfolio/market risk is volatility, which is a statistical measure (the standard deviation-SD) of the variability of return around its average value. The simplest ways to explain volatility is that if returns behaved as normally distributed random variables with average of say 10% and standard deviation of 20%, then there is a 68%, 95% and 99.7% chance that the return (R) will be within 1 SD (i.e. -10%< R <30%, range is 10% +/- 20%), 2 SD (-30%<R<50%) and 3 SD (-50%<R<70%) of expected return (10%); or 32% chance to be 1 SD (<-10% or >30%) 5% chance to be 2 SD(<-30% or >50%) and 0.3% chance to be 3 SD (<-50% or >70%) below/above the average or expected return (10%).

As indicated in the previous “What is risk?”section, volatility (standard deviation) is not only one of the most widely used and perhaps the least meaningful definitions of risk to the average investor. Volatility is not that useful because it is not that intuitive for most investors, and even for whom it has some meaning (e.g. the probability of being some number of standard deviation from the mean) is only meaningful if you assume that returns are normally distributed (a stretch at best). Furthermore the traditional volatility measure (standard deviation) doesn’t differentiate between unfavorable changes or decreases to your wealth/assets (which you’d be concerned about) and favorable changes or increases in assets (which you are not concerned about). Volatility at best is a very narrow definition of risk, and at worst it is misleading and/or irrelevant.

Some workers in the field tried to find ways to discriminate between ‘good’ and ‘bad’ variability by using “downside risk” measures such as semi-variance (which only counts negative variability from expected return in the variance calculation) or MDD (maximum draw down over a period of interest.

You no doubt have heard the oft-quoted message that the risk of equities decreases dramatically if you have a very long holding period. Those mathematically inclined will readily resonate with the reason for perceived decreased risk of stock over longer holding period is the use of standard deviation (SD) as a measure of risk. To show that the risk actually decreases with time, if the SD over one period is SD(1), then over n-period is SD(n)= SD(1)/SQRT(n). Therefore if risk or SD=20% per year then the predicted SD over 25 years is SD (25) = SD (1)/SQRT (25) =20/5=4 or a dramatic decrease in predicted risk from SD=20% to SD=4%! This concept that time reduces or eliminates risk is referred to as “time diversification”, but it is only a myth (e.g. see my Time Diversification blog.)

A somewhat different measure of risk which is a measure of intra-horizon risk is “first passage volatility”, defined as the likelihood of a certain loss over our planning horizon. This measure perhaps a little more realistic and we should be able to better relate to since it immediately leads to the question of how we’d deal with such a drop in the value of the portfolio at any point over the horizon of interest. Note, that this “first passage volatility” measure of risk actually increases over time as opposed to the traditional definition of volatility which decreases over time!…(Bartolomeo). (Later on we’ll also discuss Kritzman’s used of “turbulence” (and risk regimes) and “first passage probability” to better assess risk of a portfolio.)

Further putting doubt on the value of Volatility (standard deviation) as a risk measure, Pablo Triana in the Financial Times’ “Challenging the notion that volatility equals risk”wants to dispel the notion that volatility is a good indicator of risk. He argues (the obvious, at least in retrospect) that “volatility can provide camouflage for lethal assets”, given how easy it is to cook the numbers by simply going back a few more years and adding them if they were a period of good behaviour; this and other similar tricks mentioned indicate that “it is quite easy to use standard deviation to categorize problematic stuff as non-problematic”.

Returning to the perhaps simplest statement of risk “The likelihood of not being able to meet one’s objectives”, consider a financial planning situation which demonstrates the complications of even this simple definition. A common approach in financial planning is to evaluate the risk associated with some withdrawal level in retirement is to use a Monte Carlo simulation to estimate the probability of running out of money for some asset allocation and expected years in retirement. In a Russell research paper entitled “Mis-measurement of risk in financial planning” Richard Fullmer CFA argues that this measure of running out of money is an inadequate measure. He suggests that in general a better risk measure is the product of the probability of failure (i.e. unfavourable event or outcome) and magnitude of loss, i.e. Risk= Probability * Magnitude. However, in the context of financial planning an even better measure might be Shortfall Risk= Probability of Shortfall * Magnitude of Shortfall, i.e. it is not just the probability that a failure occurs (i.e. you run out of money) that counts, but scenarios with smaller “average conditional magnitude of shortfall” or cases where failure is occurring closer to the end of a 30 year retirement plan are less undesirable (or are more desirable) than when failure occurs many years before projected time in retirement.

So now we can go back to our earlier comment that the simplest and perhaps the most meaningful definition of (market) risk might be “the probability of not being able to meet your objectives” (e.g. unable to meet your monthly expenses, or retire at your planned age in your planned lifestyle, etc). So (market or some) event risk is not some measure of what the variability that is associated with the (market or some) event, but the impact of that event and associated variability will have on your objectives. As the saying goes, stuff happens, so what’s the impact of that ‘stuff’ on your objectives?

Dimensions of risk

When investors think of risk, they most commonly think about market risk. But investment/market risk is just one dimension of risk, which may not even be the most significant type of risk threatening an individual (depending on where they are in their life-cycle. From a life-cycle investing perspective:

TC = FC + HC i.e. Total Capital (TC) = Financial Capital (FC) + Human Capital (HC)

HC is the present value of one’s remaining lifetime work income. Typically, FC=0% (or close to it) at start of one’s working life, while HC represents (close to) 100% of a person’s TC. At retirement the situation is exactly reversed. So typically at start of one’s working life market risk is a relatively unimportant dimension of risk compared risk of death or disability. Whereas at retirement, if one is living exclusively off one’s portfolio then market, longevity and inflation risks might be dominant dimensions (and death and disability are financially less important).

In an old blog based primarily on Zvi Bodie’s writings on Life-Cycle InvestingI discuss some of the major risks one faces through one’s life-cycle:

– disability (initially most wealth is HC, so loss of earning ability can be disastrous) – death (with young family/dependents, death of primary breadwinner can lead to poverty) – investment/market (especially near the start of de-accumulation, when volatility around retirement can result in significant reduction in retirement income and/or delay in the start date of retirement) (There is a long list of (sub-)risks associated with investment/market risk such as: currency risk, credit risk, default risk, interest rate risk…etc…) – longevity (not only are people retiring earlier, but life expectancy has increased to 19 and 12 years, for 65 and 75 year olds, respectively, and is growing; of course about 50% of individuals live past the indicated life expectancy. For a 65 year old couple, there is about a 50%, 25% and 10% probability to one of them living to 90, 95 and 100, respectively).The net effect is that people are spending more time in retirement and they’ll need an income stream over a longer retirement period before exhausting their assets. – inflation (this is a scourge throughout the life-cycle, but it especially severe during retirement, eating away at your predominant financial capital). Just as iinflation is particularly corrosive for older/retired people, deflation is more damaging for young/working people (e.g. they have to repay their mortgage with more valuable dollars).

Other related risks that come to mind are:

-are you saving enough?

-if you annuitize, are you annuitizing at the right time(interest rate risk, mortality credits, costs/fees)?

-are you being overly conservative with your investments? (e.g. little or no equities in your portfolio may lead to not being able to keep up with inflation).

-are you considering Black Swan events (and tail risk) (i.e. unknown unknowns)?

Risk modeling

As mentioned earlier the most commonly discussed definition of risk is volatility (the standard deviation of return per unit of time, say a year), and assuming that the distribution of returns is normal around the mean long-term return of the market (e.g. stock market). Also mentioned earlier was that this is a slippery slope, since mathematics will quickly lead you to incorrectly conclude that stocks are riskless in the long-term. Unfortunately, even if the return distributions were normal (which they are not), you’d have to contend with intra-horizon risk; i.e. in any year between 1 to N you could encounter one of those recently observed ‘undesirable’ periods like the fall-winter of 2008 when we took a 40-70% hit depending on which market we were invested in.

There is a big difference between modeling physical behavior (as in the science of physics applicable to inanimate objects) as opposed to economic behavior(which involves humans with their aspirations, plans, fears, greed and the uncertainties/surprises that nature throws before us.)

John Kay writes in the Financial Times’ “Don’t blame luck when your models misfire” that “The source of most extreme outcomes is not the fulfilment of possible but improbable predictions within models, but events that are outside the scope of these models… There are no 99 per cent probabilities in the real world. Very high and very low probabilities are artifices of models, and the probability that any model perfectly describes the world is much less than one. Once you compound the probabilities delivered by the model with the unknown but large probability of model failure, the reassurance you crave disappears… Insurance companies do fail, but not for the reasons described in such models. They fail because of events that were unanticipated or ignored…the search for objective means of controlling risks that can reliably be monitored externally is as fruitless as the quest to turn base metal into gold. Like the alchemists and the quacks, the risk modellers have created an industry whose intense technical debates with each other lead gullible outsiders to believe that this is a profession with genuine expertise. We will succeed in managing financial risk better only when we come to recognise the limitations of formal modelling. (My emphasis) Control of risk is almost entirely a matter of management competence, well-crafted incentives, robust structures and systems, and simplicity and transparency of design.”

So keeping in mind the difference between modelling physical and economic behaviour, the difficulty to build credible models which then are further challenged by the use of parameters that change over time and the impossibility to a priori model Black Swan events (by definition), you must take financial risk models (even when packaged with sophisticated analysis by brilliant individuals back up by enormous computing power) with a large grain of salt! I like to remind myself periodically of Richard Hamming’s warning that “computing is for insight, not numbers”. So given these caveats, we can now consider some of risk models that (re-)emerged post-Great recession of 2008/9: (1) multi-regimes vs. one risk regime and (2) risk factors rather than asset classes as the analysis elements (and building blocks) rather than asset classes.

Risk regimes

In the search for new ways to tackle policy portfolios (after the perceived failure of the models previously used) based on the assumption that market behaviour can be adequately described as a normal random variable, many have suggested the need to perhaps think of the market as having multi-regimes rather than just a single-regime.

For example in the Blackrock/iShares paper “The new policy portfolio”Dopfel argued that perhaps “The wide dispersion can be explained by the presence of economic and financial market regimes—both good and bad. Each regime has distinct asset class assumptions, represented by higher or lower expected returns and volatilities” and then looked at the implications on the (institutional or individual’s) portfolio. In each regime (‘good’, bad’ and transitions), asset classes would have different characteristics. The paper demonstrates how ‘fat-tails’ and ‘skewness’ can be modeled using the sum of two normal distributions (the sum is not normal). The model includes ‘good’ and ‘bad’ states and transitions (‘good-to-bad’ and ‘bad-to-good’).The proposed models allow investors to assess their portfolio outcomes using a more realistic model and could result in new policy portfolios. This is an interesting paper which also includes mechanisms how investors might use the expectation a multi-regime environment to assess their portfolio outcomes using a more realistic model and how to create new policy portfolio.

On the same topic of unsuitability of a normally distributed representation of a single risk regime, the article “State Street identifies new approaches to managing portfolio risk” “examines the changing views of traditional practices and identifies new techniques and investment strategies that focus on measures of market turbulence, risk, liquidity and diversification” “Non-normal investment returns and dramatic swings in valuation may occur more frequently in coming years, the report states. Consequently, investors should give new consideration to within-horizon risk, investment regimes and turbulence.” “Increasingly, investors are turning to regime-specific risk analysis to form a more complete picture of portfolio risk”. Their more detailed article “Rethinking asset allocation”State Street argues that we know that the normality assumption as well as the stability of standard deviations and correlations cannot be relied upon over time, so they suggest that “investors disaggregate historical returns derived from normal periods and those associated with periods of market turbulence.” The paper also warns against disregarding within horizon risk for which investor must “understand their liquidity requirements and liability schedules” (i.e. could you continue to pay your bills and live in the lifestyle that you’re accustomed to if the market crashed during your and/or your spouse’s retirement?). The paper also addresses the universally accepted precept of diversification. Yet “most portfolios demonstrate asymmetrical correlation, with returns more diversified (i.e. uncorrelated) on the upside and considerably less (diversified, i.e. more correlated) on the downside- precisely the opposite of what most investors are seeking.” Therefore the article suggests that when sentiment is positive we should increase our allocation to risky assets, but when sentiment turns negative one should reallocate to fixed-income and cash instruments (if we only knew how to do that little market timing.) Also discussed is the importance of rebalancing, but the article points to the difficulty of doing that when the market stresses are present; as a solution at “times of high volatility and problematic liquidity”, overlay strategies are suggested whereby cash balances are equitized by using index futures. Tolerance-band rebalancing is preferred to calendar-based rebalancing, so long as the bands are selected to be appropriate for the portfolio. “Turbulence is a statistical measure designed to identify periods of unusual financial returns- either in terms of volatility or correlation, or both…periods of extraordinarily high returns could be considered just as turbulent as those of a market collapse.” Averaging correlations and standard deviations without separating out the different regimes that were involved can yield meaningless results.

And speaking of turbulence and multi-regimes, Kritzman in “Long live quantitative models” argues that “”The flaw lies not in the models but in the way less-than-careful investor implement them” and then proceeds to explain how measures of “turbulence “ and “first passage probability” would have predicted VaR (Value-at-Risk is a measure of the largest loss over some period of time with some probability (e.g. 95% or 99% of the time, i.e. 5% or 1% of the time the loss may be greater) of 35.1% (rather than 9.9% estimated naively; VaR is used mostly by large institutions to manage their overall risk, but it was not very effect measure in the 2008-2009 crash as we found out), and in fact cumulative loss during the crisis was 29.4% and maximum drawdown was 35.5%, for a portfolio of 35% U.S. stocks, 24% foreign stocks, 33% U.S. bonds, 3% real estate and 3% commodities.

Risk factors

Pimco’s Page and Taborsky in “The myth of diversification: Risk factors vs. asset classes”observe that “diversification often disappears when you need it most”. The example they give is the correlation of the Russell 3000 and the MSCI World Ex-U.S. indexes between 1970 and February 2008 had a correlation of -17%; “in contrast when both markets were down more than one standard deviation, the correlation between them was +76%”. They indicate that generally the economy oscillates between two regimes: “risk on” (“a panic driven, high volatility state characterized by economic contraction”) and “risk off” (a steady, low volatility state characterized by economic growth”). “Pimco believes asset class returns are driven by common risk factors, and risk factor returns are highly regime specific.” So risk factors should be the “building blocks” since they are the independent variables which in turn drive the behaviour of asset classes. Their analysis showed that “correlations across risk factors were lower than across asset classes” and that “the average correlation across risk factors did not increase during market turbulence.” Regimes are defined by “market turbulence” which is defined in terms of volatility and correlations (which coincide with and easier to identify by asset class returns). Interestingly both their “risk factors” and “asset classes” contained equities, real estate, commodities. However in “asset classes” we get US small cap, US large cap, global, and emerging markets, and bonds as asset classes.; whereas “risk factors” included equity, size, value, momentum and bonds were represented by their characteristics like duration, 2-10 slope, 10-30 slope, EM spread, mortgage spread, corporate spread, swap spread. “A majority of investors don’t think twice before they average their risk exposures across quiet and turbulent regimes. Consequently much of the time, investors’ portfolios are suboptimal.”

The starting point for Knut N. Kjaer in “Asset and risk management in a post-crisis market”is also risk factors, such as (p.25): real rate, inflation premium, nominal bond premium, credit risk premium, cash-flow risk premium, growth and country risk premium, size/liquidity premium, value/carry, momentum and volatility. He then argues that it is insufficient for portfolio managers to focus exclusively on asset classes, such as: T-bills, government bonds, emerging market bonds, corporate bonds, currencies, convertibles, public equity, emerging market equity, private equity, real estate, infrastructure and commodities. Risk factors must be included in portfolio construction for understanding of what is driving asset class returns. (Kjaer also sings the praises of rebalancing which he calls “the most important institutional mechanism a manager can implement to build institutional clarity…rebalancing is essential from two perspectives: it provides the discipline to avoid herd behavior and pro-cyclical investing, and it exploits mean-reversions while earning a diversification premium. It ensures diversification and mitigates risk. Rebalancing also imparts an automatic value bias because buying assets with recent price declines and selling assets with prices gains provide liquidity.”

In “Turbulence can improve portfolio diversification” Susan Wiener interviews Mark Kritzman who says that” turbulence is a statistical measure of both volatility and correlation. Volatility alone doesn’t capture enough information about interactions between assets. Also, he suggests that measures such as VIX have additional shortcomings…they are only available for asset classes that have liquid option markets, and they are forward-looking measures, so they don’t measure what’s actually going on now.” He indicates that since turbulence persists, it may be useful as an early warning signal and a signal to gradually and move partially out of risky assets since risk adjusted returns drop significantly in such times. “But his (Kritzman’s) top priority is not forecasting turbulence…but building a portfolio that will be more resilient during turbulence. (In another article Portfolios for turbulent timeshe discusses the “turbulent optimal” portfolio is heavily allocated to non-US equities (37%) as well as commodities (12%) and REITs (6%). Time will tell if we truly understand better if risk factors are superior to asset classes from a downside correlation perspective, because practically we don’t worry much about upside correlation. Upside and downside correlations are different, so for real diversification we should be looking at downside correlations (Kritzman)

Bottom line

Definitions of risk range from the mathematically convenient but not very meaningful, to perhaps meaningful but mathematically intractable; forcing one to think in terms of something simple like not being able to meet one’s objectives. So no wonder we have difficulty in measuring risk, given that there is not even a unique definition of what risk is. Volatility doesn’t cut it; neither as a definition nor as a measure of risk. The closest you might come to a meaningful definition is the probability of something bad (e.g. a shortfall) happening multiplied by the size of the shortfall. Types of risk range from known-unknowns (measurable risk) to unknown-knowns (un-measurable risk) all the way to unknown-unknowns (Black Swans). Unfortunately, only the known-unknowns category can be reliably modeled. So for most risk situations credible models are not available, parameters driving them don’t behave consistently over time (e.g. returns, standard deviations, correlations), and we are even unsure what might be the appropriate independent variables to consider (e.g. asset classes or risk factors). It’s no surprise that markets are so difficult to model, since unlike inanimate things for which physics might be appropriate (but even there not useful, as in hurricanes), behavior of markets is heavily influenced by human behavior. Unfortunately, in order to derive predictive value from risk models, you need credible models; and the state of risk modeling is considered by some to be an art and by others sorcery. Another risk categorization is that based on its dimensions; these include: death, disability, market/investment, inflation, longevity and many others. The most relevant dimensions to each individual are a function of one’s life-cycle stage. For younger individuals early in their work careers protection of their human capital against death and disability is most important, whereas inflation, longevity and market risk are most important in the near- or in-retirement stage of one’s life-cycle, when Financial Capital is predominant.

Bottom line is that definition, measurement, modeling or a complete understanding of all dimensions of risk can only be described as partial at best, and potentially misleading or wrong at worst. (I’ll have a look at risk management strategies in a forthcoming blog.