Critical Illness Insurance

In a nutshell

I am not prepared to buy a Critical Illness (CI) Insurance policy (in many ways for similar reasons I wasn’t prepared to buy Long-Term Care (LTC) policy). Among the reasons are:

-it is expensive; load factors of 40-45% are typical (i.e. for each dollar of premium only $0.55-60 benefits are paid, and for the example considered an actuarially fair premium would be about 53% of the charged premium)

-benefits are not related to cost of dealing with CI event; unlike losses associated with life, health (esp in the U.S.), home, disability and liability insurance, the CI associated financial losses would tend to be less catastrophic and already covered by good life, health and disability policies

-a better use of the premium funds might be to set up a CI account to save and invest the premiums for future (CI or discretionary)use

-if you already own a policy for about ten years, the policy continues to age 100 and premiums are fixed, you might want to investigate if it might make sense to keep it (if sunk costs are disregarded)

-policies are complex and not standardized; triggers, inclusions/exclusions are difficult to understand (though probably less so than in the case of LTCI)

(P.S. Thanks to EF and JL for suggesting the CI topic for a blog.)

What is it?

Critical illness (CI) insurance pays a specified amount (typically $25K, $50K, $75K or $100K) in case one is diagnosed with a life threatening (so not all cancer necessarily qualifies) critical illness (cancer, heart attack, stroke, and other explicitly specified conditions). This is usually cheapest when one is young and typically is not available past age 65. Not every policy has the same list of CIs upon which a payout is promised, and some policies require that insured live at least 30-90 days after diagnosis (“survival period) and/or have 90 day waiting period before cancer coverage takes effect after policy goes into force. The recommended amount varies but some sources suggest 1-2x salary. Apparently CI insurance is popular in Canada and UK, but less so in the US.

Why buy it?

It covers the white space left between life insurance (i.e. you don’t get paid unless you die) and disability insurance (you may not be sufficiently disabled to receive disability benefit and/or you may have some ‘large’ expenses coincidental with CI condition or may wish to eliminate some major debts.)

According to AIG’s “Understanding critical illness insurance ” CI claim probability is much higher than death or disability as shown in the table below (note that the higher probabilities indicated for younger individuals, is because the probability covers longer period of time to age 65)

CI benefit may cover some experimental treatment not covered by one’s health insurance policy

CI is applicable in individual (with or without dependents) or the business context (e.g. partner protection)

Other arguments in support of buying CI insurance are constructed around the data in the Some Statistical Data section of this blog below.

Why not buy?

One of the main reasons not to buy is high load factors of 35-45%; these are sometimes related to specific regulatory requirements resulting in adverse selection concerns. (‘Load factor’ of 25% means that for each $1.00 of premium only $0.75 is paid out in benefits; the complementary descriptor also used by the insurance industry is ‘Loss ratio’ which is the amount of benefits, in percent, paid out for each dollar of premium.

Another reason not to buy is that CI is sold (it’s an order of magnitude easier to find articles on ‘how to sell CI’ than why this makes sense financially or otherwise) not bought (like property and casualty, health and life insurance). Sales tools often scare tactics: “the cost of living is higher than the cost of dying” or “would you rather lose your home?”(“Critical Illness Presentation” )

Also, policy value is not related to expected costs associated with specific CI (it feels more like a lottery ticket)

Here are some quotes from “ Marketing of critical Illness insurance” material to insurance companies encouraging them to start selling CI insurance “Many clients perceive that the chances of suffering a critical illness condition are high. Whether this is correct or not is a different issue but, as such, critical illness cover addresses clients’ fears in relation to what they perceive as a high probability event. These fears are often non-specific in financial terms, although mortgage protection is a common objective. The product provides clients with peace of mind.”, and “The four great motivators are said to be greed, fear, love and obligation. To a degree, critical illness speaks to all of them.” For those interested for an in-depth look at the sophisticated sales approaches to CI insurance, this document from Munich Re, is a great read.

There is also a risk that the insurance company may not be around to pay in 10, 20 or 40 years, so check what third government guarantees may be available to secure claim.

Policy considerations (partly from “Critic al illness presentation ” )

There appears to be no standardization of:

-What CIs are included/excluded? Is list too restrictive? Some policies cover only 1-3 major CIs while other cover 20-30.

-The specific triggers to payout (‘diagnosis’) can change with evolving technology and may be challenged;

-A person may not live the (often) required 30 days after diagnosis

-Exclusion of pre-existing conditions

-Beware if premiums are not guaranteed

-Think twice about buying CI policies which are non-renewable after past age 65 (when CI incidence actually starts to rise significantly). Policy types appear to be individual/group, annual renewable with increasing rates with age, finite term fixed single/annual premium (e.g. 10 years)

-Return of premium feature/option upon death or age 100

-Is payout a function of ‘severity’ of illness?

-Do you need both disability and CI insurance?

-Is there a medical questionnaire and/or paramedical exam requirement? Pre-existing conditions (exclusions/limitations/waiting periods from policy start)

-Some policies include help with finding/accessing “world class expertise” for establishing appropriate treatment

Some Statistical Data

Figure 8 in the Gutierrez and Macdonald paper “Adult polycystic kidney disease and critical illness insurance” , based on UK data from early 90s, was the source of incidence rates I used covering all critical illnesses as a function of age/gender, that I have used. There are reports of quality issues with CI incidence data and it may also be location dependent. The CI incidence data from this paper was used as the basis of the numerical calculation in the Example shown further on in this blog. Here is the original data from the referenced paper (I used this data, after clarification from Dr. Macdonald as to its correct interpretation, to generate the probabilities used in the net present value (NPV) calculations further on in this blog. Of course, ultimately, there will be CI incidence differences between countries and CIs (and other Ts & Cs) ultimately included/excluded among different policies, so the perceived quantitative conclusions are somewhat qualitative.)

Example

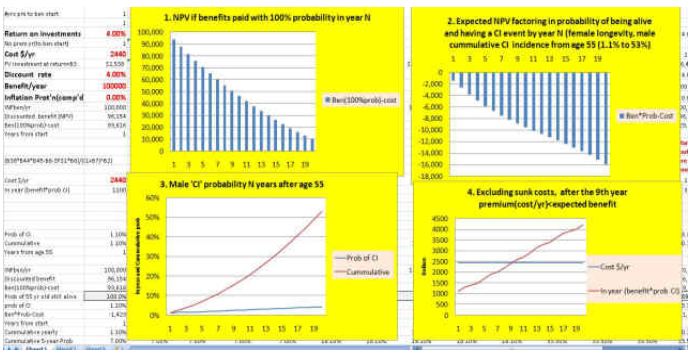

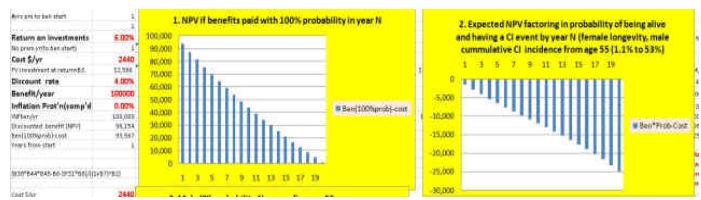

55 year old male $100,000 CI coverage, annual premium $2,440 payable to age 100 and premium paid is refundable at age 100. (All calculations disregard the impact of taxes, if any.)

Note that Graph 3, below, the blue curve is the probability of a CI event in any one year between ages 55 and 75 ;for example the probability of a CI event at age 55 is about 1.1% and increases at age 75 to 4.4% (blue curve). The red curve shows the probability of a CI event between age 55 and age 55+N; so at N=10 for example the red curve represent the probability of a CI event between age 55 and 65 is about 18% (i.e. it also indicates that between age 55 and 75 there is a 53% probability of a CI event).

Now Graph1 shows that if one is certain (100% probability) to have a CI event by age 75 (i.e. within 20 years of 55), then NPV >0 (but in reality there is only 53% probability of this as indicated in Graph 3).

Graph 2 shows that when we factor in the actual probability of both being alive and having a CI event, when you include all sunk costs at all ages (i.e. all premiums paid to date) the NPV<0 for all ages to 75 (and beyond).

Graph 4 however shows that if we discard previous sunk costs each year (i.e. disregard earlier years’ premiums paid) then it may not make sense to allow the policy to lapse after the 9th year, since the in-year premium is less that the expected in-year benefit (i.e. policy is worth keeping based on these numbers). This is because around year 9 of this policy (around age 64), when the probability of a CI event is 2.4% (and increasing each year thereafter), then the expected benefit is $2,400 (2.4% of $100,000) which is about equal to in-year premium paid ($2,440).

The following shows the identical example with expected return of 6% from a balanced portfolio (rather than the “risk free” rate of 4%). The outcomes are similar as in the 4% return case, though somewhat even less favorable.

Conclusion

The bottom line is that I am not convinced that CI insurance is a good use of my funds (NPV<0), though if you already have a CI policy for a number of years (and premiums are guaranteed) then, disregarding sunk costs, it may not make sense to cancel it. Of course if one feels that (s)he needs CI insurance for “peace of mind” or wants to place a bet (lottery) on a CI event, then it is a different consideration, so long as one realizes that it is not* an actuarially fair priced bet (because load factor is in the 40% range). Interestingly, if the annual premium was about $1,300 then the NPV would be within +/-$600 throughout the first 20 year period of this policy (i.e. it would be an actuarially fair premium).

*corrected February 5,2012 by adding the omitted word not in the last paragraph, to indicate that “it is not an actuarily fair priced bet”

Hello Peter,

A few reasons why some would want to own a critical illness policy.

One is if you are self employed.

A recent example is I had a client who had two polices for a total of $150,000. He had a heart attack and was back at work in three weeks. A disability policy (which is important to have) would not pay out.

I wrote a blog you can check out.

http://youngandthrifty.ca/critical-illness-insurance-and-why-you-need-it/

I personally own two policies myself which are term to 100 with return of premiums at death if their is no payout.

The problem with insurance is no one likes it. We insure our house for full value yet when it comes to us we like to think nothing will happen.

The other thing I would suggest is many doctors own critical illness policies themselves.