Structured Products III – Create Your Own Enhanced Index Product

In Structured Product II- Good or Bad? It Depends on Your “View” we discussed how to compare products with different performance characteristics, by using your “view” of the probability of future returns and we compared the expected outcome (value) of an enhanced index structured product with the expected outcomes of the reference index and that of a 50:50 mix of the reference index and a bond maturing at the maturity date of the structured product.

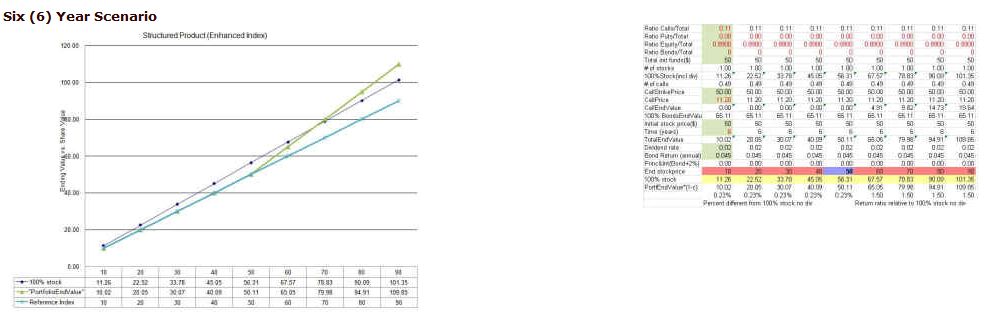

We will now proceed to build the enhanced index product which returns approximately 1.5x the return of the reference index, when that is positive, and returns 1x reference when returns are negative. To achieve that, we are looking for a way to enhance the return when it is positive. Since the initial value of the index in the example was 50, we will use a combination of calls with a strike price of $50 (i.e. the starting value of the reference index) and the index (i.e. the total return of the index-including the dividends). Let’s assume that in each example we’ll be buying calls for the approximate percentage of the assets that we can then recover with the dividend payments over the life of the structured product. Specifically, we buy calls for about 2%, 4% and 11% of the assets in our instances of structured product maturity of 1, 2 and 6 years respectively when, for simplification, dividends are constant at 2% of the maturity value of the index; the corresponding amounts invested in the index itself will then be 98%, 96% and 89% respectively, assuming no leverage. So let’s summarize what we have, assuming 2% dividends on the reference index:

We will now proceed to build the enhanced index product which returns approximately 1.5x the return of the reference index, when that is positive, and returns 1x reference when returns are negative. To achieve that, we are looking for a way to enhance the return when it is positive. Since the initial value of the index in the example was 50, we will use a combination of calls with a strike price of $50 (i.e. the starting value of the reference index) and the index (i.e. the total return of the index-including the dividends). Let’s assume that in each example we’ll be buying calls for the approximate percentage of the assets that we can then recover with the dividend payments over the life of the structured product. Specifically, we buy calls for about 2%, 4% and 11% of the assets in our instances of structured product maturity of 1, 2 and 6 years respectively when, for simplification, dividends are constant at 2% of the maturity value of the index; the corresponding amounts invested in the index itself will then be 98%, 96% and 89% respectively, assuming no leverage. So let’s summarize what we have, assuming 2% dividends on the reference index:

| Matturity of Structured Product | One (1) Year | Two (2) Years | Six (6) Years |

| Percent Allocated to Calls | 2% | 4% | 11% |

| Percent Allocated to Index | 98% | 96% | 89% |

| Call Price (Strike Price=50) | $5.00 | $7.50 | $11.20* |

*calculated to result in 1.5x enhancement to the price index using given asset mix

The 1 and 2 year call prices were obtained by looking at recently available quotes for (American) calls on the S&P 500 and the MSCI EAFE Indexes, at a strike price equal to the current value of the index (which is arbitrarily set at $50 for this example), the longer term calls (LEAPS) for 1 and 2 years were priced at approximately 10% (here $5) and 15% (here $7.5) of the current value of the S&P 500 and MSCI EAFE indexes, respectively; I could not find a quote for the 6 year (American or European) call; this was selected to result in 1.5x enhancement to the price index and then I’ll let you judge if it is sensible as compared to the 1 and 2 year American calls. One could surmise that 22% ($11.20) of current index value should be attractive to a call writer (seller); i.e. if current value of the price index is 50, the call writer gets $11.20 immediately, to give the right to the call buyer to purchase the index in 6 years for $50; possibly not a great exposure, given the index would have to drop more than 22% before losses set in.

So we look at the three scenarios, 1, 2, and 6 year maturities, with the above asset allocation, call prices and dividends. The resulting return multipliers, when returns are positive are approximately 1.2, 1.26 and 1.5 for 1, 2 and 6 years respectively. The detailed spreadsheet outputs for the three scenarios are given below.

So as you can see that you could build your enhanced indexed structured product with similar characteristics without locking in your assets for 6 years, assuming that you could buy the six (6) year calls for about $11.20 and a strike price of $50, when the initial value of the index is $50! If you believe that there is a significant upside potential in the price index, you may wish to add a small amount (5-10%) of leverage to enhance the index even more by buying more calls.