(Originally posted July 16, 2008)

Why is this important? Because over a lifetime of saving for retirement, total assets accumulated at 1.5% and 3.0% annual fees are respectively 23% and 46% lower than those resulting from 0.4% fees (Ambachtsheer and Bauer)!Or, because in retirement 1.5% extra annual cost can reduce you standatrd of living by about 30%; if annual market return corresponding to a given portfolio risk is 7.5% is used to determine your annual ability to draw income at the rate of 5% from the portfolio, then paying an extra 1.5% (say 1.8% vs. 0.3% in management fees) reduces your ability to draw income from 5% to 3.5% per year, which is a 30% reduction in annual retirement income!

As they realize the drag of (mutual fund) fees on their ability to accumulate assets for retirement or draw income in retirement, more and more people are exploring a shift to an ETF based portfolio implementation. Also, it is getting easier and easier to do this since:

-new ETFs allow you to buy highly diversified capitalization weighted basket with a single low cost ETF (e.g. Vanguard Total World Stock ETF-VT and the Vanguard FTSE All-World ex-US ETF-VEU) -discount brokers who have traditionally offered model portfolios based on mutual funds are now doing the same with ETFs (my discount broker offers six ETF based model portfolios all with <0.3% aggregate MER)

Clearly it is possible to implement a well diversified portfolio very cheaply (<0.3%). Even if you conclude that you can’t (I am not sure why) or won’t do it yourself, you should be able to get professional advice from a fee-only/based advisor at equivalent of 0.5-1.0% annual advisor fee (depending on the size of your portfolio) for a total cost of about 0.8%-1.3%.

I think that many people, who can invest a little time, can implement/manage their portfolio themselves and keep their cost-related headwinds to a minimum (even if they initially get launched with a competent fee-only/based advisor who develops an Investment Policy Statement for them). I have discussed Investment Policy Statements (your objectives, risk tolerance, and how to translate that into a financial/retirement plan), Asset Allocation and Portfolio Management under the Education tab of this website.

Let’s now look at how one might do a simple and cheap implementation of a primarily ETF based portfolio for a Canadian and a U.S. based investor, if one was starting from scratch.

I have chosen to use a 60% stock and 40% fixed income (bond plus cash) mix as the example here, because it is close to what I use and it is for someone with slightly above average risk tolerance. I discuss portfolio risk and the typical impact of portfolio mix at the end of this blog. If you have lower/higher risk tolerance you can increase/decrease the portfolio bond allocation.

Let’s first dispense with “Cash reserve” that you may wish to consider. For a working individual who is still accumulating assets for retirement you may wish to have an easily accessible cash reserve equivalent to six months of expenses in case you lose your job; your reserves should be higher if you expect to make/have some major expenses in the next couple of years (e.g. new roof, car…) or need to prepare for even higher expenditures if you are preparing to make a down-payment on a house. Let’s assume for now that 10% of the total assets are allocated to Cash.

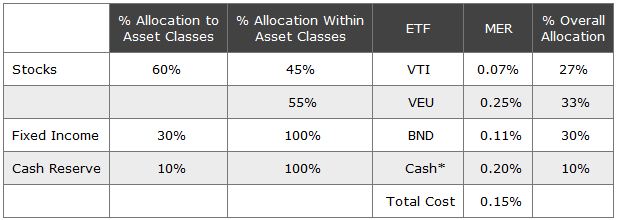

So putting it all together the Canadian investor’s simple and cheap portfolio whose risk tolerance can accommodate a 60% stock and 40% fixed income (bonds and cash), could look like:

Note that the total annual cost of this portfolio is 0.21%, plus any transaction costs that you may incur during the year. (This compares quite favorably with Canadian mutual fund MERs of 2-3 %. This difference could lead to a significantly larger portfolio or significantly lower contributions to achieve a given level of assets for retirement.) As far as currency/geographical diversification this portfolio has 58% Canadian, 18% U.S. and 24% rest-of-the-world Canadian exposure.

So putting it all together the American investor’s simple and cheap portfolio whose risk tolerance can accommodate a 60% stock and 40% fixed income (bonds and cash), could look like:

*as noted above Cash may be implemented with either Tax-exempt VMMXX or Taxable VWITX from Vanguard or other similar funds.

Note that the total annual cost of this portfolio is a low 0.15%, plus any transaction costs that you may incur during the year. As far as currency/geographical diversification this portfolio has 67% U.S. and 33% rest-of-the-world exposure. (Note that two money market funds were used here, one taxable and the other tax-exempt, but you may need to use only one of them depending on your circumstances and rates. Also you may substitute the mutual fund version VBMFX for BND with very similar results. There are similar ETFs from other vendors, like Barclays iShares and others, if you wanted to diversify ETF sources, at possibly slightly higher cost.)

Note that the total annual cost of this portfolio is a low 0.15%, plus any transaction costs that you may incur during the year. As far as currency/geographical diversification this portfolio has 67% U.S. and 33% rest-of-the-world exposure. (Note that two money market funds were used here, one taxable and the other tax-exempt, but you may need to use only one of them depending on your circumstances and rates. Also you may substitute the mutual fund version VBMFX for BND with very similar results. There are similar ETFs from other vendors, like Barclays iShares and others, if you wanted to diversify ETF sources, at possibly slightly higher cost.)

You can read more about how to build your portfolio in Chapter 13- Defining Your Mix in William Bernstein’s “The Four Pillars of Investing” (The availability of ETFs was relatively limited when this book was published, so most references are to mutual funds, but the concepts are still valid and the explanations are clear.

Additional considerations:

Additional considerations:

-assuming that you are starting with all cash/fixed-income portfolio and you are planning to retarget to a different mix, then it is advisable (especially is you are re-deploying a significant amount of money) is to do it, not all at once, but over a period of time; for example 1/3 of the funds could be redeployed every 2-3 months.

-one would typically prefer to hold fixed income in tax-deferred (CAN:RRSP, US: 401(k), IRA, etc) or tax-free accounts (CAN: TFSA(start in 2009), US: Roth IRA). -if you are moving a tax-sheltered account from one institution (e.g. from your full service broker or bank) to another (e.g. to your online discount broker) make sure that assets are NOT de-registered (get the assistance of the receiving broker who will no doubt will be willing to assist you with transfer) so that you are not hit with an unnecessary tax-bill

-in accumulation phase one may wish to keep emergency reserve equivalent of 6-12 mo expenses in cash equivalents; during retirement one may wish to hold equivalent of 2-years expenses in cash/short-term bonds to minimize need to sell assets at distressed prices. (The Cash Reserve would likely be in the taxable account, though one could conceive circumstances where it may be in the tax-free or tax-deferred account)

-if you are not starting from scratch, but you already have mutual fund , stock, bond and GIC/CD investments you need to develop a plan how to move to the new ETF based implementation while minimizing taxes (if not in a tax-deferred or tax-free account one may try to offset capital gains/losses) and expenses (transaction costs, deferred sales charges, etc)

-you’ll note that all ETFs used to implement foreign assets are un-hedged editions of the funds, so you will be exposed to the impact of not just returns in local currency, but also currency exchange variations (which can enhance or detract from returns, but also increase diversification)

-Market conditions change and that may affect the specific choice of taxable or tax-exempt money market or bond funds for American investors; if fund is for tax-exempt/deferred portion of the portfolio, then the taxable fund should be used as it usually has a higher yield, if however the fund is for the taxable portion of the portfolio, then depending on the investors tax bracket the taxable or tax-exempt fund may yield higher after tax return.

-on the bond asset class, one could use a ladder of 1- 5 year GIC (Canada) or 1-5 year CD (U.S.) in addition to or instead of the bond ETF, depending on the rate differences and the acceptability of the risk of not having access to the money.

-for instances when a low –cost versions of an asset are available both in mutual fund form and ETF as for example American investors can access Vanguard Total Bond Index either as a mutual fund VMBFX (MER=0.19) or and ETF like BND (MER=0.11), then additional consideration should be given to the transaction cost (likely zero for VMBFX and $10-$30/transaction for the ETF) if automatic monthly investments are made.

-when an investor is in accumulation mode and ETFs are used to implement the portfolio asset allocation, you may need to temporarily hold your contributions/savings for 2-3 months in a money market account before it is transaction cost efficient to buy the ETFs; this is not an issue for the retired decumulating investor as most transactions are likely an annual sale of assets necessary to cover expenses for the year (not already covered by private/public pensions or cash-flow from dividends/interest)

-as your portfolio grows you can start thinking of more elaborately diversified portfolio with a sprinnkling of other asset classes (REITs, Commodities, Gold…)

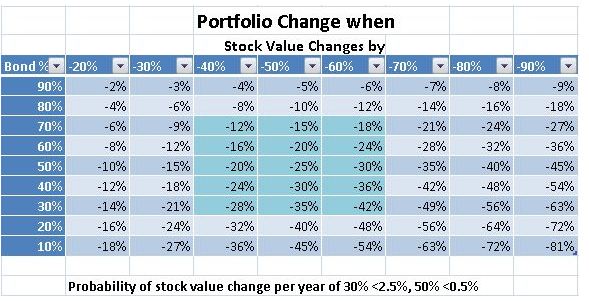

Risk Tolerance First let’s look at the change in a portfolio’s value as a function of percent loss on the stock portion of the portfolio, for various levels of fixed-income (bonds and cash) component in the portfolio (which are assumed to stay unchanged when the stocks lose value).

Risk Tolerance First let’s look at the change in a portfolio’s value as a function of percent loss on the stock portion of the portfolio, for various levels of fixed-income (bonds and cash) component in the portfolio (which are assumed to stay unchanged when the stocks lose value).

As you can see from the following table, the portfolio loss can range from minimal to significant. One’s risk tolerance is dependent on one’s ability and willingness to take risk. You’ll recall that a bear market is when there is a 20% drop from the previous peak but since 1945 there were two bear markets that exceeded 40% peak-to-trough losses.

I have chosen to use a 60% stock and 40% fixed income (bond plus cash) mix as the example above, because it is close to what I use and it is applicable for someone with slightly above average risk tolerance. For the U.S. stock market under normal distribution assumptions there is <2.5% probability of 30% annual loss. Even two of those 30% loss years back to back would “only” result in about 50% stock component drop (hopefully less than that with the geographical diversification), and a corresponding 30% portfolio loss for the 60% stock and 40% bond/cash portfolio. Changing this mix you can change to a portfolio of different level.