Hot Off the Web- August 1, 2011

Personal Finance and Investments

In the Globe and Mail’s “The difference between advisers and counsellors” John Heinzl looks at the difference between financial advisers (typically commissioned salespersons (though there is a move toward asset based pricing) like brokers, account execs, stock brokers wealth advisers, etc) and investment counsellors. Henzl indicates that working with an investment counsellor “Also known as a portfolio manager, these firms or individuals generally have rigorous educational and ethical standards, typically work with higher net-worth individuals and also often manage money for foundations, endowments, pension funds and other institutions.” Some of the differences from advisers he lists are: asset based fees (1-2%), discretionary management, fiduciary duty, larger accounts (>$500,000); he also includes a set of questions to ask before signing up. The website of the Portfolio Management Association of Canada has a list its members. (You still need to convince yourself that the incremental cost of active management over a low cost ETF based portfolio is worthwhile)

In the Financial Post’s “Falling off fixed income ladder hurts”Robert Cable writes that staying with short maturities in the expectation of ‘imminent’ higher interest rates for the past few years has hurt investors’ returns on fixed income securities (GICs/CDs, bonds). So he argues that instead of basing the investment decision on a guess on the direction of future interest rates, it makes more sense to return to the old tried-and-true ladder “one- through five- year maturities) beats almost any other strategy 19 times out of 20”. Based on his example “The “fall off the ladder” investor has to be 1) right on the direction of interest rates, 2) right on the magnitude of the increase in the level of interest rates, 3) right on the timing of the increase in interest rates and if he somehow manages to get all of this right then … he will actually simply break even with what he would have earned by simply staying with the discipline of the ladder. If you’re at all wrong on any factor, you lose. You have to get everything right just to break even.”

In the Financial Post’s “Who takes care of your money when you can’t?” Jonathan Chevreau explores “What happens to retired boomers who succumb to Alzheimer’s disease or other forms of dementia but who still manage their own portfolios through online discount brokerages? With no human financial advisor to act as intermediary, is there not potential to inflict massive portfolio losses with a few ill-chosen clicks of a mouse? What if they’re single, divorced or widowed and there’s no spouse to notice their declining mental capacity?” Referring to a new BMO report on the subject which indicates that: “cognitive abilities actually decline” with age, “those suffering from dementia may not even be aware of it”. The importance of estate planning should rise in importance to wealth creation. Recommendation mentioned is the creation of a ContinuingPower of Attorney (CPOA) which unlike a regular POA (for property or health) “remains in place even if the grantor becomes incapacitated”, specifically if grantor is medically certified as no longer able to manage own affairs. CPOA would bypass the need for a court appointed guardian. (No solution offered to the problem of single individuals with nobody to identify declining mental capacity.)

Real Estate

The May 2011 Canadian Teranet House Price Index indicates that “Canadian home prices in May were up 1.3% from the previous month, according to the Teranet-National Bank National Composite House Price Index…It was also the sixth consecutive monthly rise, coming after three straight monthly declines. As in April, prices were up in all six of the metropolitan markets surveyed. The May gain was 1.6% in Vancouver and Toronto, 0.7% in Montreal, 0.6% in Calgary, 0.5% in Ottawa and 0.1% in Halifax….The 12-month gain of the composite index in May was 4.4%, the same as in April. The largest 12-month rise was 6.3% in Montreal, followed by 6.2% in Vancouver, 5.6% in Ottawa, 4.8% in Halifax and 4.6% in Toronto.”

The May 2011 U.S. “S&P/Case-Shiller Home price Indices” indicates that ”The 10- and 20-City Composites were up 1.1% and 1.0%, respectively, in May over April. Sixteen of the 20 MSAs and both Composites posted positive monthly increases; Detroit, Las Vegas and Tampa were down over the month and Phoenix was unchanged. In May 2011, the 10- and 20-City Composites recorded annual returns of -3.6% and -4.5%, respectively.” On a seasonally adjusted basis the May 2011 10- and 20- city composites essentially show no change in the month, at 0.1 and 0.0%, respectively. In the LA Times’ “Home prices rise again, but experts are unimpressed” (Thanks to CFA Institute Financial NewsBriefs) Alejandro Lazo writes that “Prices often rise in spring because of changes in the types of homes selling: Foreclosures make up a higher proportion of sales during the winter as families take a break from home shopping and cash-rich investors dominate the market. Higher sales volumes in spring also push up prices. But compared with May 2010, home prices slid 4.5%, according to the index released Tuesday…S&P has warned that the adjusted data are unreliable because the high number of distressed properties has distorted the market.” Wesley Lowery is less than enthusiastic about the data in WSJ’s “Home sales, prices reflect malaise” where he reports that “Separately, the Census Bureau reported Tuesday that new-home sales fell 1% in June from a month earlier to an annual rate of 312,000 units. That was weaker than many economists were expecting and puts the current sales pace below last year’s total of 323,000 sales, which was the lowest annual total on record. Economists said the housing market continues to be hampered by tight lending standards that are keeping buyers on the sidelines as well as high unemployment—the national rate now stands at 9.2%. The political battle between Republicans and Democrats in Washington over raising the debt ceiling has injected fresh worries to the market. Consumers, wary that borrowing costs could increase, are canceling purchase contracts and delaying making a decision until the situation in Washington is resolved.”

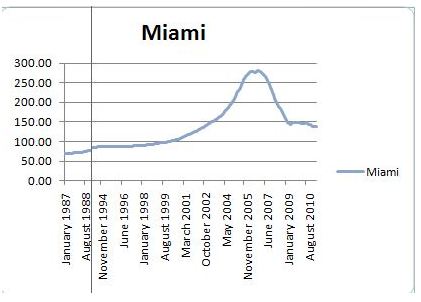

As far as Florida trend is concerned, a graphical view of the Case Shiller data for Miami, readily shows that prices are back to late 2002 levels, but still above the 1987-2000 trend-line.

In WSJ’s “What sort of insurance do I need?” June Fletcher discusses the insurance protection recommended/required on Florida beach property, especially for those on an island. Unlike other states, in Florida there is significantly higher risk of hurricanes, tornadoes and floods, and therefore you can expect to pay significantly higher insurance rates than on a primary residence in a northern state. The state owned Citizens Property Insurance will cover those who are unable to secure wind/hurricane insurance from private companies. Flood insurance is also needed in coastal/island areas. Also mentioned are mould and fungi insurance, though companies have become more restrictive on such coverage. Replacement rather than depreciated cost coverage is recommended. You should shop around as there is competition, and discounts are available on insurance if you take steps to mitigate the risks (e.g. hurricane windows and/or shutters.) (You might want to discuss with your insurance agent whether flood insurance is required if you are on a higher floor in your beach condo.)

Pensions

Mark Cobley reports in the Financial News’ “Lehman Nortel pensions case goes to Court of Appeal” that the case brought by UK Pension Regulator opened last week to answer the “question of where a company’s pensioners rank in the queue of creditors. If the firm goes bankrupt, do the pensioners get paid before banks who have lent the company money?” (Of course UK pensioners have their pensions guaranteed up to about $50,000 by the UK Regulator and the battle is about the regulator recovering the pension shortfall ahead of other creditor. Canada is apparently the only OECD country (beside Portugal) that has neither a pension insurance fund (except a minimal one in Ontario guaranteeing to top up the shortfall on the first $1,000/mo pension) nor any priority over other unsecured creditors in case of sponsor bankruptcy, leaving private sector pensioners completely exposed to inadequate, incompetent and conflicted sponsors, administrators, regulators and supporting professionals like actuaries, investment managers, custodians, etc)

In the Financial Times’ “OECD report shows pension costs and returns vary widely” Sara Silver reports on the availability of a new OECD report on pensions entitled “Retirement-income systems in OECD and G20 countries”. Silver indicates that “The OECD found the costs of running pension funds varied widely across developed nations, ranging from 0.1 per cent of plan assets in Denmark and Portugal to 1.3 per cent in Spain and 1.4 per cent in the Czech Republic. Costs ran higher on average in less-developed countries, reaching a high of 5.9 per cent of plan assets in Ukraine.”

Things to Ponder

The Economist’s “The absence of leadership in the West is frightening- and also rather familiar” explains very simply Europe’s and America’s problems, the root cause of why the problems are still not resolved and recommends some reasonable paths going forward. “In the early days of the economic crisis the West’s leaders did a reasonable job of clearing up a mess that was only partly of their making. Now the politicians have become the problem. In both America and Europe, they are exhibiting the sort of behavior that could turn a downturn into stagnation. ..Europe’s politicians need to implement not just a serious restructuring of the peripheral countries’ debts but also a serious reform of their economies, to clean out cronyism, corruption and all the inefficiencies that hold back their growth. America’s Democrats need to accept entitlement cuts and Republicans higher taxes.” (Thanks to CFA Institutes Financial NewsBriefs for recommending)

Jeff Rubin writes in the Globe and Mail’s “Fed can’t keep long-bond rates from rising” that “…with each passing week, there seems to be more news of distress in government debt markets as governments grapple with record deficits… Not surprisingly, the bond market is getting nervous. There is already is a four-percentage point difference between the U.S. Treasury’s cost of borrowing in the Federal Reserve board controlled money market and the long bond market…Faltering growth and a near double-digit national jobless rate may keep the federal funds rate grounded for another year. And failure to come to grips with the deficit, and another energy-price driven point or so rise in an already 3%+ inflation rate will see U.S. long Treasury yields reach new heights this year. But according to the Financial Times Lex column’s “U.S. downgrade: reasons for indifference” but since “There are few other places to go. And in any case, would buying elsewhere be clever? Investors may have spotted an ironic twist: a US downgrade might cause Treasuries to rally as riskier assets were dropped. A bet against the richest and most powerful country on the planet is never a safe one. On the same subject, the WSJ’s “Gauging the fallout from a U.S. downgrade” David Wessel writes that “A prediction, widely shared in Washington and on Wall Street: One month from now, Congress will have lifted the federal debt ceiling, the U.S. government will be paying its bills, the president will have signed a convoluted deficit-reduction law that defers decisions on benefits and taxes—and the U.S. will have lost its AAA credit rating…Ultimately, the issue is the unsustainable fiscal trajectory of the U.S. government and the inability of the political system to change course. The credit rating isn’t the problem. The problem is the problem.”

In Bloomberg’s “SEC’s Stanford Ponzi ruling provokes clash with investor fund’Schmidt and Gallu report that the SEC ordered the SIPC (Securities Investor Protection Corp., the industry run investor protection group) to start paying Stanford investors up to $500,000. The SEC argues that in the same way as in the Madoff case, Stanford’s Ponzi scheme’s victims should be compensated. “Under the 1970 Securities Investor Protection Act, if a broker absconds with, say, 100 shares of stock, SIPC will replace it for the client. SIPC also will cover missing cash, up to $250,000 within a $500,000 cap per customer. SIPC doesn’t cover investment losses, however, even when they come from securities fraud. That’s an issue at play in the Stanford matter.”

In the Financial Times’ “ESMA calls for tighter ETF rules”Chris flood reports that the European Securities Market Authority (ESMA) has proposed comprehensive new rules for the operation of ETFs. The proposal includes requirement for disclosure on: “…how their funds track an index and the issues that could contribute to tracking errors, such as transaction costs, illiquid components or dividend flows. And it proposes giving investors in synthetic ETFs more information on the type of collateral provided by counterparties, the risk of a counterparty default and the effect on returns. Another question is whether synthetic ETF providers should be required to hold collateral that closely matches the assets of the index an ETF aims to track. Esma also wants providers to state clearly if they are engaging in securities lending, say how any lending revenue is shared with lending agents, what collateral they accept, and how any cash collateral is reinvested. In addition, it asks whether there should be limits on the amount of assets that can be lent by an ETF.”

The Palm Beach Post’s Susan Salisbury in “AARP selling names for millions” writes that “Most people think of AARP, the senior citizen advocacy group, as a way to get discounts on everything from dining and entertainment to insurance. What is not well-known is that the non-profit formerly called the American Association of Retired Persons makes more than $650 million a year in royalties for delivering its 40 million members to businesses, according to a congressional report issued in March….(the report expressed) concerns about whether AARP’s priority is serving seniors or its own interests.” ” According to a AARP spokesperson “AARP’s taxable subsidiary, AARP Services, works with providers to make products available in the marketplace that uniquely meet the needs of the 50-plus and offer them good value…” (There have been previous warning shots suggesting that the AARP might not be working in the best interest of its members, e.g. in my March 2, 2008 blog “In “Sure it’s from AARP. But is it a good deal?” BusinessWeek’s Anne Tergesen reminds readers to stay vigilant because on comparing AARPs annuities, life insurance and mutual funds with other options, many can do better. Just because an organization is non-profit, that is not a guarantee that it operates in the best interest of its members or even when they do their recommendations are good for you. At times it may be simply due to incompetence, at other times it may be that the organization has lost its compass and starts operating in a manner focused on self-perpetuating itself and/or its management.” There were other instances when policy positions were taken which might make many seniors wonder in whose interest the AARP is working for, such as: support of Florida’s discriminatory property taxes resulting from Save-Our-Homes amendment and the recent position on potential Social Security cutbacks.)

And finally, in Bloomberg’s “Preparing Americans for death lets hospices neglect end of life” Peter Waldman discusses potential conflicts that hospices might have between their role of “preparing people to die”, not to “prepare them to live”. “As hospice care has evolved from its charitable roots into a $14 billion business run mostly for profit…Providers have been accused of boosting their revenues with patients who aren’t near death and not eligible for hospice — people healthy enough to live a long time with traditional medical care. In hospices, patients give up their rights to “curative” measures because they are presumed to be futile…The government’s suspicions about providers have been fuelled by rising costs and lengthier patient stays.” A series of examples involving large for-profit business operations, raise serious questions about the suitability of for-profit corporations to run hospices.