Pfau: “Safe savings rates: A new approach to retirement planning over the lifecycle”

In a nutshell

Pfau extends William Bengen’s analysis of SAFEMAX (safe maximum withdrawal rates over a 30 year retirement) to the accumulation phase and defines a SAFEMIN (safe minimum savings rate through one’s 30 working years necessary to deliver 50% of one’s final year salary over a 30 year retirement). I suspect he is onto an improvement, not just in the sense that he drives the action upstream where one still has more flexibility to increase the level of savings, but also because he shines a light at the sustained high level of savings required to generate a certain retirement income. The author views as his principal contribution the maximum value of “the life-cycle-based minimum savings rate needed to finance desired expenditures (LMSR)”, which is 16.6%/yr for 30 years to generate an inflation adjusted 50% final salary replacement rate.

The details

Wade Pfau in the Journal of Financial Planning’s “Safe savings rates: A new approach to retirement planning over the life cycle”turns normal financial planning upside down. His retirement planning exercise shifts from setting a target asset size necessary to secure the intended retirement income with a 4% (SAFEMAX) annual withdrawal, to setting an annual minimum savings target (SAFEMIN) which will allow a withdrawal of inflation adjusted 50% of final year of salary. Pfau argues that rather than just focusing on the decumulation phase (retirement) with a SAFEMAX (Maximum Withdrawal Rate-MWR, typically 4%), it might be better to look holistically at the entire accumulation and decumulation cycle; his conclusion is that the real focus must start with the SAFEMIN (Minimum Savings Rate-MSR). “When considered as a whole, the historical data show that, though the relationship is not perfect, the lowest MWRs (which give us our conception of the safe withdrawal rate) tend to occur after prolonged bull markets.” He uses historical data starting with 1871 and looks at rolling 60 year periods, 30 accumulation followed by30 decumulation years. “Withdrawal amounts are defined as a replacement rate from final pre-retirement salary. I assume that the baseline individual wishes to replace 50 percent of her final salary with withdrawals from her accumulated wealth. This 50 percent is more than it may initially sound, as it is only the part from retirement savings.” This is because it excludes items like Social Security and pension income.

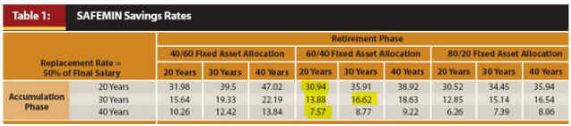

The asset allocation stays constant at 60/40 throughout retirement with annual rebalancing. The article shows the link between stock market valuation at retirement (as measured by the “10-year average of real earnings divided by the real stock market index value at the beginning of the retirement year (E10/P)”) and maximum withdrawal rates and minimum savings rates. Of course, it also assumes that the historical relationships will continue to hold. “When this smoothed earnings yield is low, the stock market tends to be overvalued as a result of a recent run-up in stock prices. Stock price appreciation helps the worker reach her wealth accumulation goal with a lower savings rate. At the same time, an overvalued stock market at the retirement date, as represented by the low smoothed earnings yield, is also correlated with a lower subsequent MWR for the new retiree.” The author views as his principal contribution the maximum value of “the life-cycle-based minimum savings rate needed to finance desired expenditures (LMSR)”, which is 16.6%/yr for 30 years to generate an inflation adjusted 50% final salary replacement rate. For those retiring between 1900-1980 the LMSR ranged from about 9.34-16.62. He concludes with the following table summarizing SAFEMIN Savings Rates:

You can readily observe what savings rate was required historically over 20/30/40 years to deliver inflation adjusted 50% of final year salary for the following 20/30/40 years, and the effect of asset allocation on these savings rates. Some of the SAFEMIN savings rates are staggering even at the 50% replacementlevel, and they demonstrate the importance of starting to save early. (The other message not mentioned in the paper, but stares you in the face, is the value of having access to a low-cost (pure) longevity insurance product, which not only insures a lifetime income stream, but also allows one to focus on a 20 year retirement phase (the approximate joint life expectancy of a 65 year old couple. The approximate cost of such insurance is less than the saving achieved by reduction of retirement phase from 30 to 20 years.) Increasing the replacement rate from 50% to some other number just requires increasing the SAFEMIN proportionately.

The assumptions used in this paper include that: future will be similar to the past, fees are assumed to be zero (a 1% fee would increase the 16.62% SAFEMIN to 22.15%…imagine what mutual fund fees of 2-2.5% will do to the SAFEMIN number!), constant real salary during accumulation (this low-balls most individual’s SAFEMIN), and withdrawals in retirement are constant in real terms (a little flexibility here allowing a decreased income in poor market years would allow somewhat lower SAFEMINs).

Conclusions

Pfau tackles the rolling 60 year accumulation/decumulation phases using over a century of historical data. He concludes that you must start saving early (a saving period of 30 years) and a lot more than you think (16.6%) to achieve even as little as inflation adjusted 50% of final salary (i.e. saving 33% for 30 years to secure 100% income replacement); and of course this is not guaranteed! (Is anything guaranteed in life?) While the findings might be a little late for the early boomers, these results are very useful to younger boomers and gen-X and gen-Y aged individuals.

His study also drives home the impact of market valuations at retirement and corrosive effects off fees on retirement income.

A great paper, which puts some meat on the determination of realistic savings rates required to achieve certain retirement income targets.